How to Invest for Retirement Amid Market Uncertainty

From President Biden’s announcement that he will not be seeking re-election, to a rotation out of tech stocks and into small caps, recent events have added to market uncertainty. The S&P 500 recently declined 2.9% from its all-time high, while the Nasdaq pulled back nearly 5%. It’s natural for investors to be concerned about where the market is headed, especially as the presidential election season heats up and the Fed prepares for its first rate cut this cycle. However, history shows that it’s important for investors to stay focused on the long run and not overreact to every news headline. More than ever, staying levelheaded is the best way to achieve long-term financial goals.

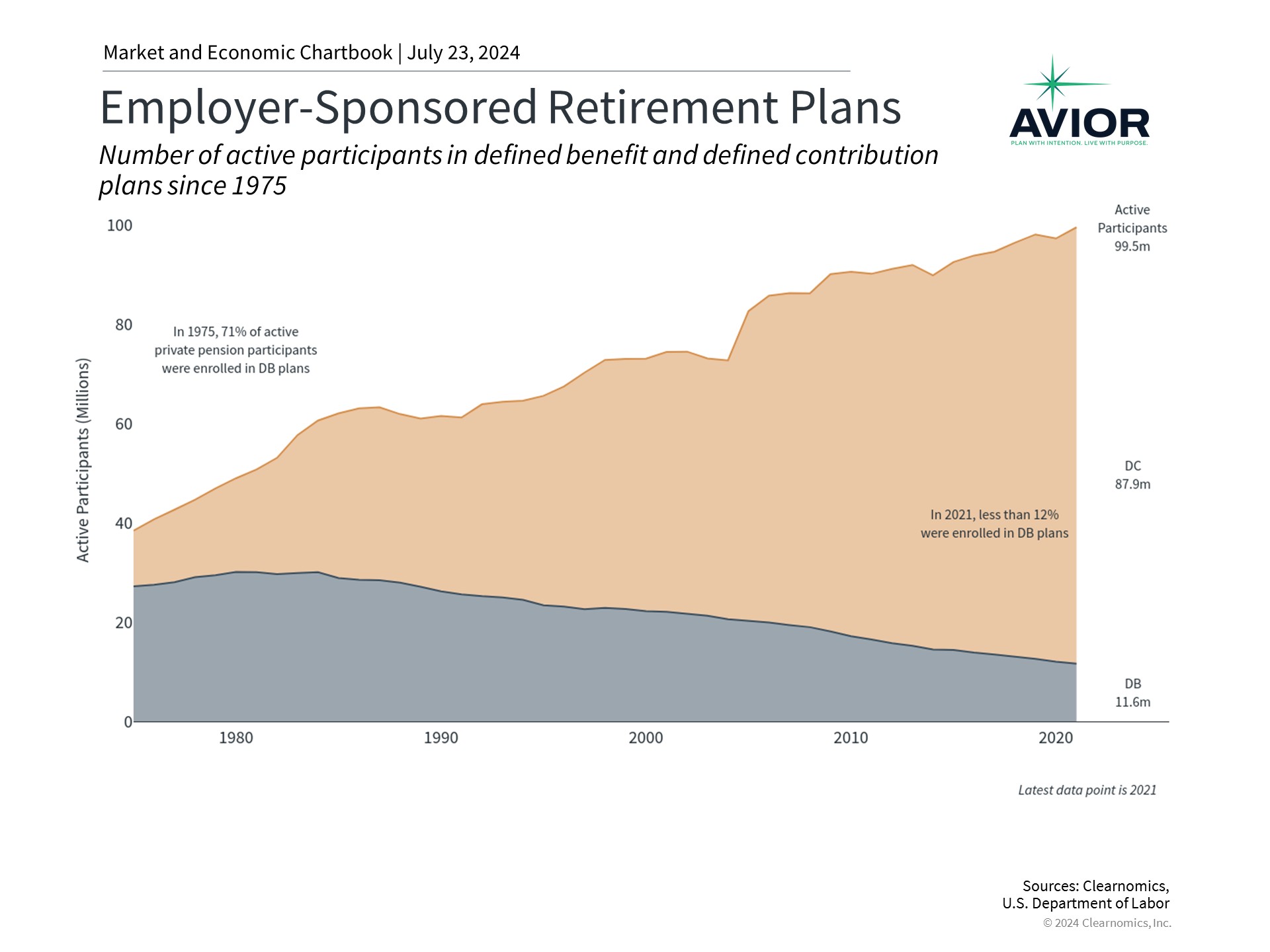

Investors are increasingly responsible for their own retirements

This is especially true when it comes to saving for retirement. For those with decades until retirement, it’s critical to start early and hold the right mix of assets that can generate sufficient growth. For those in or near retirement, sticking to an asset allocation that supports income needs while providing growth for longer retirement periods has never been more important. In both cases, investors today need an understanding of the retirement landscape and why they may need to take action to grow and protect their retirement savings.

Over the past 50 years, the burden of planning for retirement has shifted from corporations and the government to individuals. Understanding the labyrinth of investment vehicles, tax consequences, how to construct an appropriate portfolio, as well as what to do in times of market volatility can be challenging for even the most sophisticated investors. This is one reason to always seek professional advice to ensure that you’re on track to achieve your financial goals. In fact, most companies also use financial advisors to set up and manage their employer-sponsored retirement plans.

How has the retirement landscape shifted? Looking back, the American Express Company (a railroad business at the time) introduced the first pension plan in 1875. This kicked off a trend of employers providing benefits for employees in retirement. For much of the next century, these were largely “defined benefit” plans, meaning employers contributed to a shared fund and eligible employees would receive benefits in a set amount once they became eligible. Defined benefit plan participants would have the assurance that if they met the qualifications, they would be able to count on regular paychecks in retirement.

Of course, when most people think of receiving checks in retirement, government programs such as Social Security are what come to mind. Social Security was introduced in 1935 when the Great Depression caused unemployment to soar to over 25%. It began providing income to workers once they turned 65 and was responsible for mainstreaming the idea of a retirement age and providing a safety net for older Americans.

However, it’s widely known that shifting demographics and longer life expectancies have put the future of the program in jeopardy. According to the latest report by the Trustees of the Social Security and Medicare trust funds, Social Security reserves are expected to be depleted in 2035 unless Congress acts, at which point fund income will be sufficient to cover only 83% of scheduled benefits. It’s been the case for decades that individuals cannot simply rely on Social Security for their retirement needs.

Investors must determine the most appropriate asset allocation for their goals

Today, the investing journeys for most individuals begin with their company’s defined contribution plans, such as a 401(k) or 403(b). The key difference is that defined contribution plan participants must select and manage investments themselves. As a result, they receive benefits in retirement from only what they have saved and invested, unlike under a traditional defined benefit pension plan. The same is true for other retirement vehicles that individuals can open on their own, such as IRAs.

Given this broad shift over the past half-century, the burden of investing properly now falls squarely on the shoulders of individuals. For this reason, it is essential for all individuals to understand the key principles of investing, especially because they are not typically taught in school.

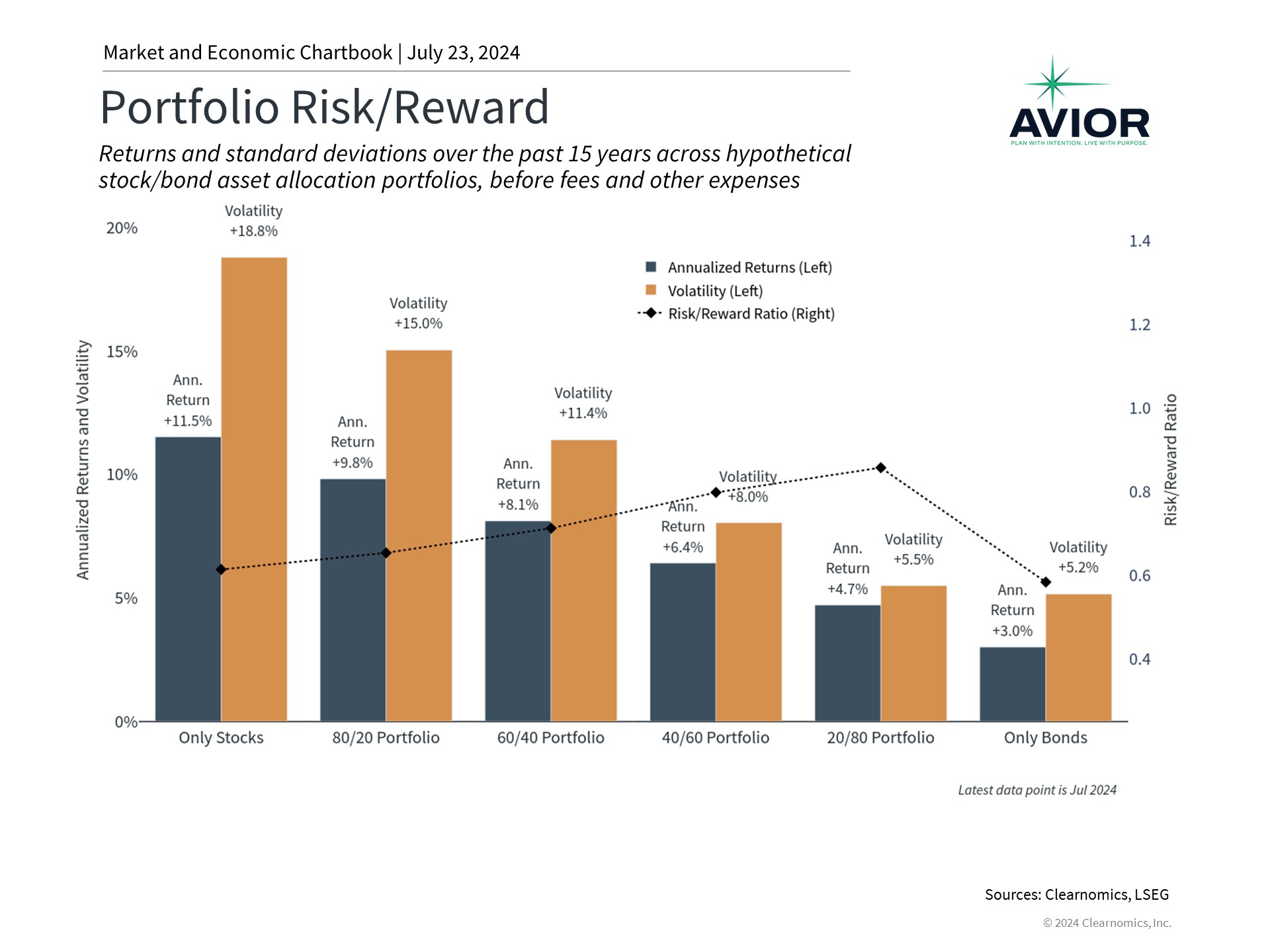

First, investors should hold a properly constructed portfolio tailored to their specific needs, including their life stage, risk tolerance, and more. In the short run, choosing the right mix of assets can help investors to weather the inevitable market swings that occur quite often, such as during the market pullbacks that have occurred throughout this year.

For example, stocks tend to generate larger returns but are also much riskier, as shown in the accompanying chart. In contrast, bonds are typically more stable but also have less potential upside. An appropriate asset allocation allows investors to take advantage of the positive attributes of both asset classes to create a portfolio that is more than the sum of its parts. Investors can then adjust this asset allocation throughout the various stages of their lives and as they approach retirement, in addition to making tactical and strategic shifts based on market conditions.

Starting early and staying invested are critical for retirement

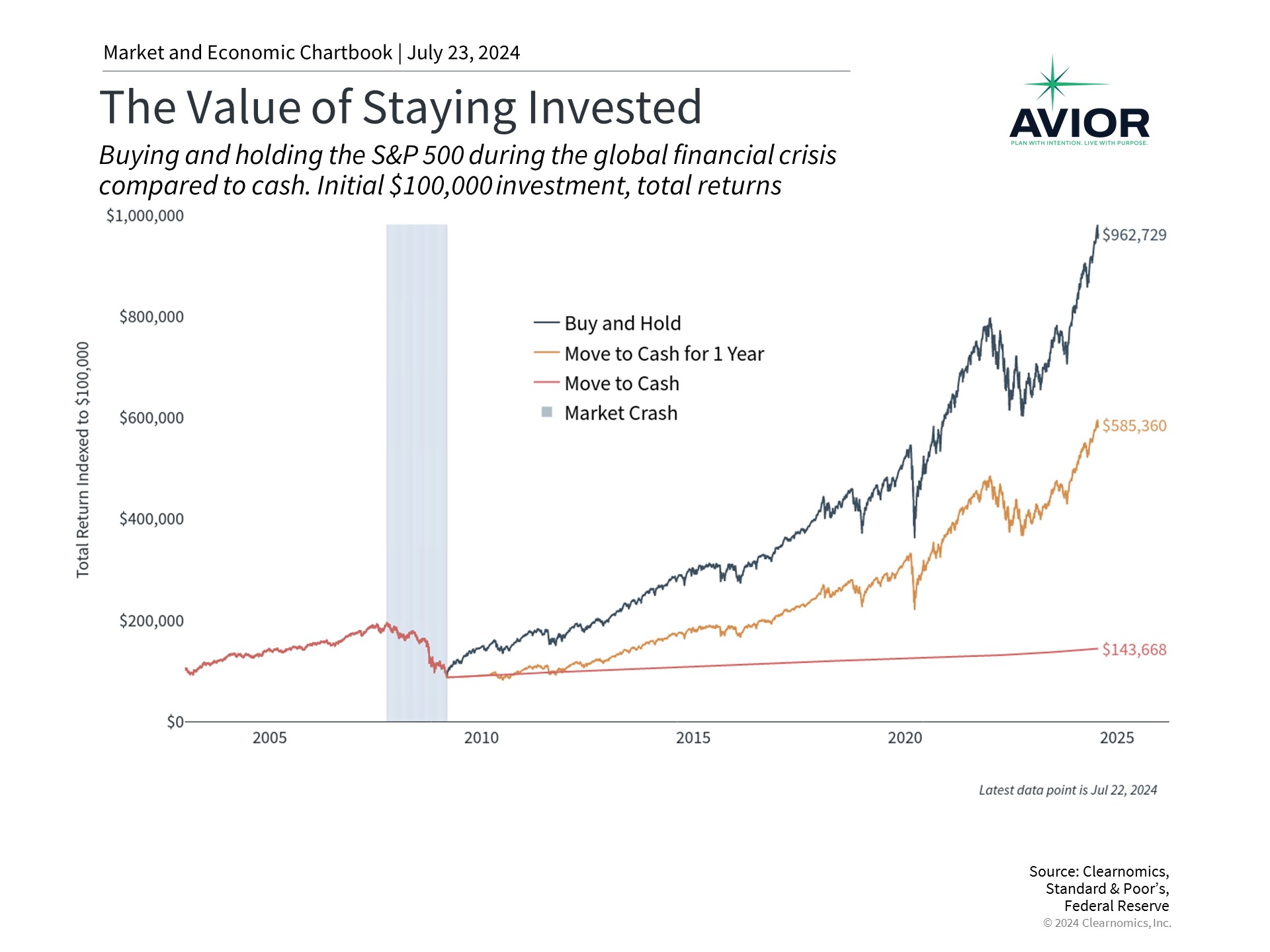

Second, saving early can help investors build wealth due to the power of compounding. The earlier an individual begins investing, the more time their money has to grow before withdrawals are needed. This is true even during periods of market turbulence such as over the past few years. While staying out of the market or keeping cash in a checking account may feel safe, the true opportunity cost is the forgone gains that could have helped to provide a more secure retirement.

Finally, it’s important to always stay focused on the long run rather than worrying about day-to-day market fluctuations. Investing early and staying invested through the ups-and-downs of market cycles are the best ways to achieve financial goals. Trying to time the market or make sudden changes to a portfolio is not only difficult but can be counterproductive since it derails investors from their true objectives.

It can often feel as if there is always another crisis on the horizon whether due to politics, the Fed, interest rates, or tech stocks. However, while there are no guarantees when it comes to investing, history shows that investors who save steadily and follow these key principles will be in a better position to grow their retirement savings.

The bottom line? Today’s retirement landscape requires individuals to take responsibility for their own financial planning. While this is challenging, it also creates opportunities for investors to tailor their retirement plans to their specific needs.

Disclosure: This report was obtained from Clearnomics, an unaffiliated third-party. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.aviorwealth.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. Please remember to contact Avior, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian. A copy of our current written disclosure Brochure and Form CRS (Customer Relationship Summary) discussing our advisory services and fees continues to remain available upon request or at www.avior.com.

No Comments

Sorry, the comment form is closed at this time.