How Much Does Long-Term Care Really Cost? A 2025 Breakdown

Long-term care is one of those expenses most people hope they’ll never need, but statistics tell a different story. About 70% of seniors will need some type of long-term care during their lifetime, yet many families are caught off guard by the costs when the need arises. With 10,000 Baby Boomers turning 65 every day until 2030, understanding these costs is essential for anyone planning their financial future.

In 2024, the national annual median cost of a semi-private room in a skilled nursing center rose to $111,325, an increase of 7%, while a private room jumped 9% to $127,750. But nursing homes are just one piece of the long-term care puzzle. From in-home care to assisted living, the range of options comes with an equally wide range of price tags, and understanding these costs can help you make informed decisions about your future care needs and financial planning.

Key Takeaways

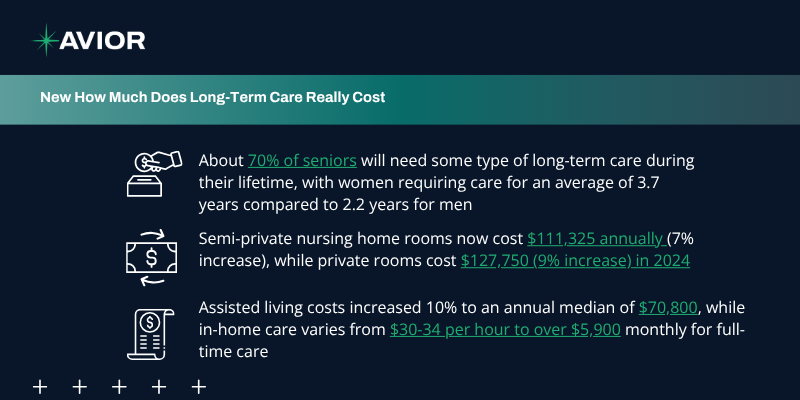

- About 70% of seniors will need some type of long-term care during their lifetime, with women requiring care for an average of 3.7 years compared to 2.2 years for men

- Semi-private nursing home rooms now cost $111,325 annually (7% increase), while private rooms cost $127,750 (9% increase) in 2024

- Assisted living costs increased 10% to an annual median of $70,800, while in-home care varies from $30-34 per hour to over $5,900 monthly for full-time care

- Geographic location dramatically impacts costs, with nursing home rates ranging from $5,639 monthly in Texas to $31,282 in Alaska

- Long-term care insurance premiums range from $900-$1,700 for single men and $1,500-$2,700 for single women for policies providing $165,000 in benefits

- 10,000 Baby Boomers turn 65 daily until 2030, creating unprecedented demand that continues driving costs higher

2025 Long-Term Care Cost Breakdown by Type

Understanding the full spectrum of long-term care costs helps you plan more effectively and choose options that fit both your needs and budget. Each type of care serves different needs and comes with distinct cost structures.

Nursing Home Care

Nursing homes provide the most comprehensive level of care, including 24-hour medical supervision, personal care assistance, and rehabilitation services. This high level of care comes with the highest price tag. In 2024, the national annual median cost of a semi-private room in a skilled nursing center rose to $111,325, representing a 7% increase from the previous year.

Private rooms command even higher prices, with costs increasing 9% to $127,750 annually. On a monthly basis, this translates to approximately $9,277 for a semi-private room and $10,646 for a private room nationally.

It’s important to note that these figures represent median costs, meaning half of all facilities charge more and half charge less. Premium facilities in expensive markets can cost significantly more than these averages.

Assisted Living

Assisted living provides a middle ground between independent living and nursing home care, offering personal care services, meals, and social activities while maintaining some independence. Assisted living community costs increased by 10% to an annual national median cost of $70,800 per year.

This breaks down to approximately $5,900 per month nationally, though costs vary significantly by location and amenities. Monthly assisted living costs include rent, three nutritious meals a day, scheduled activities, and medication management services.

Many assisted living communities offer different apartment sizes and amenities, which can affect pricing. Studio apartments typically cost less than one-bedroom or two-bedroom units.

In-Home Care

In-home care offers the flexibility of receiving services in your own home, ranging from basic homemaker services to skilled nursing care. While home health aide costs rose just 3% in 2024, homemaker services rose 10%.

The national median hourly rate for in-home care varies by service type, but most home care agencies require a weekly minimum of seven hours, with some offering up to 24-hour or live-in care options. For reference, the industry standard for “full-time” care is 44 nonsleeping hours per week, which equates to $5,900 a month based on national median hourly rates.

Adult Day Care

Adult day care provides supervised activities and care during daytime hours, allowing caregivers to work or take breaks while ensuring their loved ones receive appropriate care and socialization. This option typically costs significantly less than residential care options and can be an excellent solution for families managing work and caregiving responsibilities.

Geographic Variations in Long-Term Care Costs

Location plays a massive role in long-term care costs, with some states costing three to four times more than others for the same level of care. Understanding these variations can help with both planning and decision-making about where to age.

Most Expensive States

Alaska consistently ranks as the most expensive state for long-term care. Monthly median costs for a semiprivate nursing home room in Alaska reach $31,282, while the annual cost for a semi-private room reaches $364,452.

Other high-cost states include Oregon, Hawaii, and Washington D.C. These markets face challenges including high labor costs, limited supply of facilities, and expensive real estate markets that drive up operational costs.

Most Affordable States

On the opposite end of the spectrum, Texas offers some of the lowest nursing home costs at $5,639 monthly for semi-private rooms, with annual costs around $65,700. Missouri and Oklahoma also rank among the most affordable states for long-term care.

For assisted living, Wyoming has the lowest costs at $3,642 per month, while the District of Columbia has the highest at $7,250 per month.

Why Location Matters

These geographic differences reflect local economic conditions, including labor costs, real estate values, state regulations, and market competition. When planning for long-term care, consider whether relocating to a lower-cost area might be feasible and desirable for your situation.

Factors Driving Cost Increases

Several factors contribute to the rising costs of long-term care, and understanding these drivers helps explain why costs continue outpacing general inflation.

Labor Shortages and Wage Pressure

The long-term care industry faces significant staffing challenges, with high turnover rates and difficulty recruiting qualified workers. There are only 1.7 million assisted living employees in the U.S. to care for the 3.9 million residents, highlighting the staffing shortage.

These labor shortages force facilities to increase wages and benefits to attract and retain staff, costs that are ultimately passed on to residents and their families.

Increasing Demand

The aging of the Baby Boomer generation creates unprecedented demand for long-term care services. Every day until 2030, 10,000 Baby Boomers will turn 65, and seven out of ten people will require long-term care in their lifetime.

This demographic shift means demand for services will continue growing faster than the supply of facilities and caregivers, putting upward pressure on prices.

Regulatory and Quality Requirements

Long-term care facilities must meet extensive regulatory requirements for staffing, safety, and quality of care. While these regulations protect residents, they also increase operational costs that contribute to higher prices.

The COVID-19 pandemic also introduced new safety protocols and requirements that add to operational expenses.

Planning and Payment Options

Understanding costs is only half the equation – you also need to know how to plan for and pay for these expenses when they arise.

Long-Term Care Insurance

Long-term care insurance can help cover the costs of extended care services. According to the 2023 price index, for policies that provide $165,000 in benefits, single men paid anywhere from $900 to $1,700, while single women paid from $1,500 to $2,700.

The gender difference in pricing reflects women’s longer life expectancy and higher likelihood of needing long-term care services.

Government Programs

Medicaid covers long-term care for individuals with limited income and assets, but eligibility requirements are strict. Medicare provides limited coverage for skilled nursing care and home health services but doesn’t cover long-term custodial care.

Veterans and their spouses may be eligible for VA benefits that can help cover long-term care costs.

Self-Funding Strategies

Some families choose to self-fund long-term care costs through savings, investments, or home equity. This approach requires careful planning to ensure adequate resources will be available when needed.

Family Caregiving

Many families provide care themselves, though this approach has both emotional and financial costs that should be considered in planning.

Future Cost Projections

Long-term care costs show no signs of slowing their upward trajectory. Current projections suggest continued increases that will outpace general inflation.

Industry experts predict that demographic trends, labor shortages, and increasing care complexity will continue driving costs higher. If current projections hold, the monthly cost of a semiprivate room in a nursing home will be approximately $11,077 by 2030, an increase of 15.9 percent.

These projections emphasize the importance of planning early and considering multiple funding strategies to address future long-term care needs.

Work With Us

Long-term care costs represent one of the largest potential expenses in retirement, yet they’re often overlooked in financial planning. With costs ranging from tens of thousands to over $100,000 annually depending on the type and location of care, and 70% of seniors likely to need some form of long-term care, these expenses can’t be ignored. The key is understanding your options and developing a strategy that protects both your care preferences and your financial security.

At Avior, we help clients navigate the complex landscape of long-term care planning, from understanding insurance options to developing comprehensive funding strategies that protect family wealth while ensuring quality care. Our team stays current on the latest cost trends and policy changes, helping you make informed decisions about long-term care insurance, asset protection strategies, and family planning approaches. Don’t let long-term care costs derail your retirement security – contact Avior today to develop a comprehensive strategy that addresses both your care preferences and financial goals, ensuring you’re prepared for whatever the future may bring.

Investment management and financial planning services are offered through Avior Wealth Management, LLC, an SEC-registered investment adviser. Tax and accounting services are provided by Avior Tax and Accounting, LLC, a wholly-owned subsidiary of Avior Wealth Management, LLC.

Insurance products, including life, disability, long-term care, and annuities, are offered through Avior Insurance. Insurance and annuity products are not offered through Avior Wealth Management, LLC, and are not covered by SIPC. Avior Insurance operates independently to provide insurance solutions tailored to clients’ needs. Insurance products are subject to the terms and conditions of the issuing carrier.

All information contained herein is general in nature and is not to be construed as specific investment advice. Avior does not provide legal advice. Clients should consult their own legal, tax, and financial professionals before making any decisions. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results.

No Comments

Sorry, the comment form is closed at this time.