Integrating Estate Planning with Your Retirement Strategy

You’ve spent decades building your retirement nest egg. Your 401(k) is funded, your IRA is growing, and you’ve run the numbers countless times. But there’s a critical piece missing from your retirement puzzle – what happens to all that money after you’re gone? More importantly, what happens to your family if something happens to you before retirement?

Most people treat retirement planning and estate planning like separate projects handled by different professionals at different times. This disconnect creates a disconnect that can cost families hundreds of thousands in unnecessary taxes, probate fees, and lost wealth. When retirement and estate planning work together as an integrated strategy, you maximize what you keep during your lifetime and what you pass to the next generation.

Key Takeaways

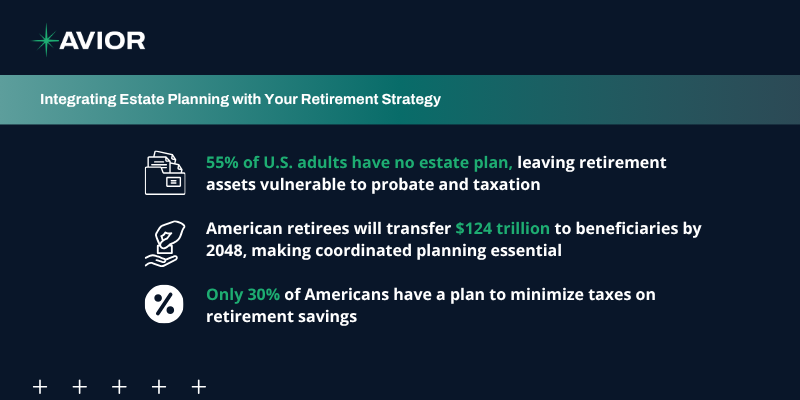

- 55% of U.S. adults have no estate plan, leaving retirement assets vulnerable to probate and taxation

- American retirees will transfer $124 trillion to beneficiaries by 2048, making coordinated planning essential

- Retirement account beneficiary designations override wills and trusts, requiring careful coordination

- Only 30% of Americans have a plan to minimize taxes on retirement savings

- Required minimum distributions from retirement accounts affect both retirement income and estate taxation

- Integrated planning can reduce estate taxes, avoid probate, and help ensure smooth wealth transfer

Why Retirement and Estate Planning Must Work Together

Your Largest Assets Need Coordinated Protection

For most families, retirement accounts represent the largest assets they’ll ever own. 401(k)s, IRAs, pension plans, and other retirement vehicles often exceed the value of homes, investment accounts, and other property combined. These accounts operate under complex rules that differ from other assets, creating unique planning challenges.

Retirement accounts have their own beneficiary designations that bypass wills and trusts entirely. A perfectly crafted estate plan becomes worthless if your retirement account beneficiaries contradict your other estate documents or create unintended tax consequences for your heirs.

Tax Implications Span Both Strategies

Retirement planning focuses on minimizing taxes during your lifetime, while estate planning aims to minimize taxes at death. These goals can conflict without proper coordination. Strategies that reduce current income taxes might create massive estate tax problems, while estate tax reduction techniques could trigger unnecessary income taxes during retirement.

Only 30% of Americans have a plan to minimize taxes on retirement savings, and even fewer understand how retirement account taxation interacts with estate taxation. This knowledge gap costs families billions in avoidable taxes every year.

The Beneficiary Designation Trap

Why Wills Don’t Control Retirement Accounts

Your will controls assets titled in your name – your house, your car, your bank accounts. But retirement accounts aren’t controlled by wills at all. They transfer directly to named beneficiaries through contractual arrangements with the account custodian.

This means you could create a comprehensive estate plan, hire the best attorney, and establish a perfect trust, only to have your retirement accounts – often your largest assets – go to the wrong people because you forgot to update a beneficiary form you filled out decades ago.

Common Beneficiary Mistakes

The most common mistake is naming minor children directly as beneficiaries. When minors inherit retirement accounts, courts must establish guardianships and conservatorships to manage the money. This creates exactly the court involvement and expense that estate planning should avoid.

Another frequent error is failing to update beneficiaries after major life events. Divorced spouses, deceased parents, or estranged family members often remain as beneficiaries simply because no one updated the forms. Only 46% of will executors were aware of a will, suggesting similar communication gaps exist with beneficiary designations.

Required Minimum Distributions and Estate Planning

The RMD Factor

Required minimum distributions force you to withdraw money from traditional retirement accounts starting at age 73. These mandatory withdrawals affect both retirement income planning and estate planning. Large RMDs push you into higher tax brackets, increase Medicare premiums, and reduce the amount available to pass to heirs.

Estate planning strategies can reduce RMD impacts through Roth conversions, qualified charitable distributions, or strategic withdrawal sequencing. These tactics require years of advance planning, not last-minute scrambling when RMDs begin.

Inherited IRA Rules

The SECURE Act changed how beneficiaries inherit retirement accounts. Most non-spouse beneficiaries must now empty inherited IRAs within ten years, potentially creating enormous tax bills. This “tax bomb” can push heirs into the highest tax brackets for a decade, destroying much of the inherited wealth.

Proper integration of estate and retirement planning can spread this tax burden through strategic Roth conversions before death, careful beneficiary selection, or trust structures that provide more control over distributions.

Roth Conversions as Integration Strategy

Converting for Estate Planning Benefits

Roth conversions involve paying taxes now on traditional IRA funds to create tax-free growth going forward. While often viewed as a retirement planning strategy, Roth conversions provide powerful estate planning benefits too.

Heirs inherit Roth IRAs tax-free, eliminating the income tax burden on inherited retirement accounts. This proves especially valuable for beneficiaries in high tax brackets or those inheriting large accounts that would otherwise trigger massive tax bills.

Strategic Timing Matters

The best time for Roth conversions is during low-income years before RMDs begin or between retirement and age 73. These windows allow you to convert at lower tax rates while creating tax-free inheritance for your family.

Converting in small amounts over multiple years keeps you in lower tax brackets and avoids pushing yourself into higher Medicare premium tiers or triggering other income-based penalties.

Trusts and Retirement Accounts

When Trusts Make Sense as Beneficiaries

Most estate plans include trusts to control asset distribution and protect beneficiaries. However, naming trusts as retirement account beneficiaries requires careful planning because of complex IRS rules governing trust distributions.

Conduit trusts pass all RMDs directly to beneficiaries, maintaining simplicity but providing limited protection. Accumulation trusts allow more control but can trigger higher taxes. The wrong trust structure can turn a tax-advantaged inheritance into a tax disaster.

Special Needs Beneficiaries

Families with disabled beneficiaries face unique challenges. Direct inheritance of retirement accounts can disqualify beneficiaries from government benefits. Special needs trusts must be carefully structured to preserve both government benefits and retirement account tax advantages.

These situations require coordination between estate planning attorneys, tax advisors, and financial planners so that all rules are followed correctly.

Charitable Giving Integration

Qualified Charitable Distributions

Retirees aged 70½ and older can donate up to $105,000 annually directly from IRAs to qualified charities. These qualified charitable distributions count toward RMD requirements while excluding the amount from taxable income.

This strategy integrates retirement planning (satisfying RMDs), tax planning (reducing taxable income), and estate planning (fulfilling charitable intentions) in a single transaction.

Charitable Remainder Trusts

For larger estates, charitable remainder trusts allow you to donate retirement assets to charity while providing income to beneficiaries for years or even decades. The charity receives the remainder after the income period ends, but beneficiaries enjoy income along the way.

These trusts eliminate estate taxes on the donated portion while providing income tax deductions and ongoing income streams. They work particularly well for large retirement accounts that would otherwise create tax problems for heirs.

Life Insurance as Integration Tool

Replacing Taxable Retirement Income

Life insurance can replace the after-tax value of retirement accounts, allowing you to spend retirement funds freely while still leaving an inheritance. Since life insurance death benefits are income-tax-free, this strategy can actually increase what heirs receive.

This approach works especially well when retirement accounts would otherwise create large tax bills for heirs. You pay the income taxes during your lifetime when you’re in lower brackets, and heirs receive tax-free insurance proceeds.

Paying Estate Taxes

For large estates subject to estate taxes, life insurance can provide liquidity to pay the tax bill without forcing heirs to liquidate assets. Insurance held in irrevocable life insurance trusts keeps death benefits outside your taxable estate while providing cash when needed.

Coordinating Healthcare Directives

Powers of Attorney for Retirement Accounts

Estate planning includes healthcare directives and powers of attorney for financial decisions if you become incapacitated. These documents must specifically address retirement accounts to avoid complications.

Financial powers of attorney should include explicit authority to make retirement account decisions, roll over accounts, change beneficiaries if appropriate, and take distributions. Without this specific language, family members may be unable to manage your retirement accounts during incapacity.

Long-Term Care Planning

Long-term care expenses can devastate both retirement and estate plans. Costs exceeding $100,000 annually quickly deplete retirement savings meant for both your lifetime and your heirs’ inheritance.

Integrated planning addresses long-term care through insurance, self-funding strategies, or Medicaid planning that protects assets while ensuring care. These strategies protect retirement accounts while preserving your estate plan’s effectiveness.

Working with Professional Teams

Why Multiple Advisors Need Coordination

Estate planning attorneys, financial advisors, tax professionals, and insurance agents each bring specialized knowledge and experience. However, their recommendations must work together rather than conflict with each other.

The best outcomes occur when your professional team communicates regularly, understands your complete financial picture, and coordinates strategies across all planning areas. This requires initiative from you or a lead advisor who helps keep everyone working toward common goals.

Regular Review and Updates

Retirement and estate plans aren’t “set it and forget it” documents. Tax laws change, family circumstances evolve, and asset values fluctuate. Annual reviews are important to see if your integrated strategy remains effective and adapts to changing conditions.

Major life events – marriages, divorces, births, deaths, or significant wealth changes – require immediate planning updates to maintain coordination between retirement and estate strategies.

Work With Us

Retirement planning and estate planning aren’t separate projects handled by different advisors at different times – they’re two sides of the same wealth management coin. The families who preserve and transfer the most wealth are those who understand that every retirement decision has estate planning implications, and every estate planning choice affects retirement confidence.

At Avior, we specialize in coordinating all aspects of your financial life into a comprehensive strategy that maximizes wealth during retirement while preserving assets for future generations. Our team works alongside your estate planning attorney and tax professionals to help ensure retirement account beneficiaries align with your estate plan, required minimum distributions are tax-optimized, and Roth conversion strategies benefit both your retirement and your heirs. Whether you’re just starting retirement planning or need to integrate existing plans more effectively, we provide the coordination that turns separate strategies into an integrated wealth preservation system. Contact Avior today to discover how integrated retirement and estate planning can protect more of what you’ve built and help your legacy lasts for generations.

No Comments

Sorry, the comment form is closed at this time.