Inherited Accounts 101: What Families Should Know Before Filing Season Ends

Death is rarely convenient, and neither is the tax paperwork that follows. When a loved one passes and leaves behind an IRA, a 401(k), or another retirement account, the inheritance arrives wrapped in rules that most families have never encountered, rules that changed significantly in 2020 and again in 2025 in ways that are actively catching people off guard. The accounts themselves may represent decades of careful saving. How those accounts get distributed, and when, determines how much of that wealth actually stays in your family.

The stakes are higher than most heirs realize. With more than $100 trillion expected to flow to heirs through 2048, inherited retirement accounts have become one of the central vehicles for generational wealth transfer in this country. The families who understand the rules, who know which withdrawal schedules apply to them, what penalties attach to missed distributions, and how to spread income across years to avoid tax spikes, keep far more of what they receive. Filing season is a useful forcing function to get this right.

Key Takeaways

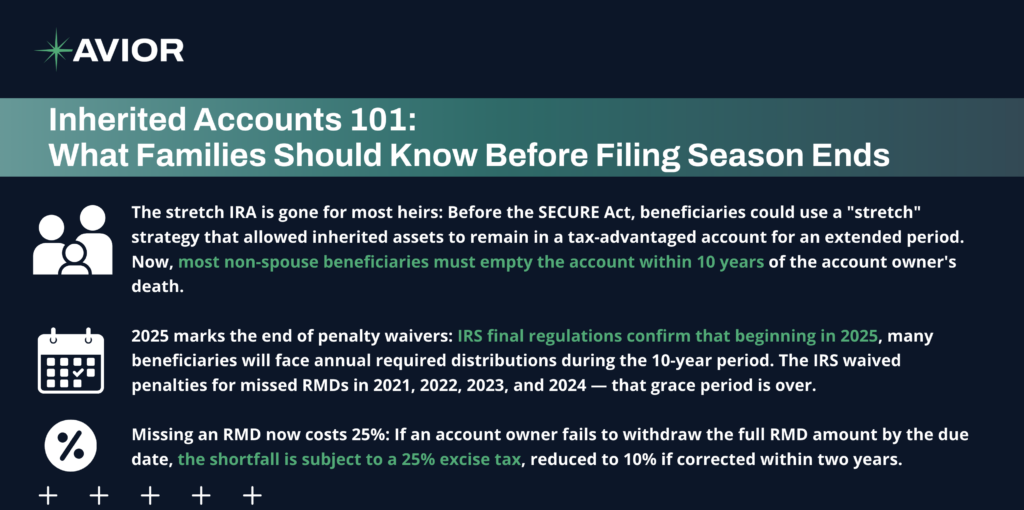

- The stretch IRA is gone for most heirs: Before the SECURE Act, beneficiaries could use a “stretch” strategy that allowed inherited assets to remain in a tax-advantaged account for an extended period. Now, most non-spouse beneficiaries must empty the account within 10 years of the account owner’s death.

- 2025 marks the end of penalty waivers: IRS final regulations confirm that beginning in 2025, many beneficiaries will face annual required distributions during the 10-year period. The IRS waived penalties for missed RMDs in 2021, 2022, 2023, and 2024 — that grace period is over.

- Missing an RMD now costs 25%: If an account owner fails to withdraw the full RMD amount by the due date, the shortfall is subject to a 25% excise tax, reduced to 10% if corrected within two years.

- Spouses operate under different rules: Surviving spouses have the option to roll the inherited account into their own IRA, which resets RMD timing based on their own age and retirement date rather than the deceased’s schedule.

- The 10-year clock started at death, not in 2025: The 10-year clock for a beneficiary who inherited between 2020 and 2023 still starts the year after death. No penalties applied for missed distributions in those years, but those years still count toward the 10-year window.

- Roth inherited IRAs still require distributions: Inherited Roth IRAs fall under the same 10-year rule for most non-spouse beneficiaries, though qualified distributions remain tax-free if the original Roth was open for at least five years.

Understanding Who You Are as a Beneficiary

The Two Categories That Change Everything

The rules governing an inherited retirement account depend entirely on your relationship to the person who died. The IRS divides beneficiaries into two broad groups: Eligible Designated Beneficiaries, who receive more favorable treatment, and everyone else, who falls under the 10-year rule. Eligible Designated Beneficiaries include surviving spouses, children under age 21, disabled or chronically ill individuals, and beneficiaries no more than 10 years younger than the account owner. If you fit one of those categories, you may still have the option to take distributions over your lifetime rather than within a compressed 10-year window.

Adult children, the most common heirs, generally do not qualify as Eligible Designated Beneficiaries. A 50-year-old inheriting a parent’s traditional IRA faces the 10-year rule, meaning the entire account balance must be distributed by December 31 of the tenth year following the parent’s death. That timeline, combined with the tax consequences of drawing down a large pre-tax account quickly, requires advance planning that many families are skipping.

Whether the Original Owner Had Started RMDs Matters

Within the 10-year rule, a critical distinction determines whether annual distributions are required in years one through nine or whether you can defer everything until year ten. If the original owner died before their RMD start date, beneficiaries do not have to take annual RMDs and can choose to wait until year ten, receive yearly distributions, or skip years, as long as the account is fully emptied by the end of the 10-year period. If the original owner died on or after their RMD start date, annual RMDs must begin the year after death and continue through year nine, with the remaining balance distributed by year ten.

This distinction has enormous practical consequences. An heir who inherited from a parent already taking RMDs must take annual distributions in years one through nine and distribute the remaining balance by year ten. An heir who inherited from a parent who died before reaching RMD age has far more flexibility to let the account grow and choose the timing of withdrawals strategically. Knowing which situation applies to you is the first step toward building a distribution plan that minimizes tax exposure across the full decade.

The 2025 Rule Change and What It Means for You

Four Years of Waivers Are Over

From 2021 through 2024, the IRS repeatedly waived the excise tax on missed annual RMDs from inherited accounts, citing confusion over how the new rules applied. That series of waivers created a false sense of security for many heirs, who interpreted the absence of penalties as flexibility that did not actually exist. As research suggests, beneficiaries who skipped distributions during those years effectively shot themselves in the foot, they received a free pass on the penalty, but the 10-year clock kept running the entire time.

Starting in 2025, specific heirs must begin taking annual RMDs or face a 25% penalty on the amount they should have withdrawn. That fee can be reduced to 10% by withdrawing the correct RMD amount within two years and filing Form 5329. For families who inherited accounts in 2020 and took no distributions during the waiver years, the account balance is now larger, and the remaining years to distribute it are fewer. The combination of a compressed timeline and a larger balance creates a real risk of income bunching in the final years, pushing heirs into higher tax brackets precisely when the distributions are largest.

The Catch-Up Problem

Heirs who missed annual distributions in 2021 through 2024 are not required to make up those specific amounts; the IRS confirmed there is no retroactive penalty for those years. However, beneficiaries who have missed RMDs from inherited IRAs since 2020 face significant catch-up requirements and must take multiple years’ worth of RMDs in 2025 to avoid penalties on those amounts going forward. The practical consequence is that some beneficiaries face a larger taxable distribution in 2025 than they anticipated, and the ripple effects on income tax, Medicare premiums, and other income-tested benefits deserve careful attention.

The Spouse’s Distinct Advantage

Rolling Over Into Your Own IRA

Surviving spouses have an option that no other beneficiary receives: the ability to roll the inherited account into their own IRA rather than maintaining it as a separate inherited account. This option resets the distribution timeline entirely. Instead of facing a 10-year drawdown based on the deceased spouse’s death date, the surviving spouse can defer distributions until they themselves reach RMD age, currently 73 under SECURE 2.0. For a surviving spouse who is significantly younger than the deceased, this rollover can extend tax-deferred growth by years or even decades.

The decision to roll over versus maintain the account as inherited is not automatic and deserves analysis. A surviving spouse who is under age 59½ and needs access to the funds may prefer to maintain the account as inherited, since distributions from an inherited IRA carry no 10% early withdrawal penalty regardless of the beneficiary’s age. A rollover into a personal IRA, by contrast, subjects early withdrawals to the standard penalty until age 59½. Choosing between these two paths requires an honest assessment of current income needs, long-term tax projections, and the surviving spouse’s own retirement account balances.

Managing the Tax Consequences of a 10-Year Drawdown

Why Spreading Distributions Across Years Usually Wins

The 10-year rule creates a default incentive to defer distributions as long as possible, letting the account grow tax-deferred while postponing taxable income. For many heirs, that instinct is partially right but incomplete. Taking more out each year can result in less total tax, withdrawing only the minimum from a large traditional IRA could leave a substantial balance in year ten, causing a significant income spike precisely when the full account must be emptied. A more thoughtful approach involves modeling the heir’s expected income across all 10 years, identifying which years have lower marginal rates due to career changes, retirement, or other fluctuations, and deliberately accelerating distributions in those lower-income years.

Inherited Roth IRAs Require Attention Too

Heirs sometimes assume that inheriting a Roth IRA creates no immediate tax concerns because Roth distributions are generally tax-free. The 10-year rule still applies. A non-spouse heir who inherits a Roth IRA must fully distribute the account within 10 years of the original owner’s death, even though those distributions carry no income tax. The strategic implication is real: an heir who delays all distributions until year ten loses the additional years of tax-free growth inside the account without gaining any tax benefit from the delay. For large inherited Roth balances, allowing the account to compound across the full 10 years before withdrawing everything in a lump sum is a legitimate strategy — but it should be a deliberate choice, not the result of inaction.

Practical Steps to Take This Filing Season

Confirm Your Beneficiary Classification and Account Details

Before anything else, identify whether the original account owner had already begun taking RMDs at the time of death. This single fact determines whether annual distributions are required in years one through nine or whether you have more flexibility over the 10-year window. If you inherited between 2020 and 2024 and have taken no distributions, count the years carefully, the 10-year clock started the year after the original owner’s death, not in 2025. Determine what year your 10-year window closes and work backward to understand how much flexibility you have remaining.

If your account custodian has not provided you with a calculated RMD for 2025, request one proactively. The rules governing inherited IRAs after 2019 are complex enough that many custodians have not yet built automated RMD calculations for these accounts, and the responsibility for taking the correct amount falls on the beneficiary, not the institution. A missed distribution because the custodian failed to provide guidance is still a missed distribution in the IRS’s view.

Work With Us

Inherited retirement accounts sit at the intersection of tax law, estate planning, and family financial complexity, and the rules governing them changed more dramatically in the past five years than in the previous three decades combined. The end of IRS penalty waivers in 2025, the full implementation of the 10-year rule, and the distinct treatment of eligible versus non-eligible beneficiaries all create decisions that deserve professional guidance rather than guesswork. Getting the distribution strategy right, whether that means spreading withdrawals across low-income years, evaluating a spousal rollover, or simply calculating the correct 2025 RMD before a penalty accrues, can preserve a meaningful amount of the wealth your family was left.

At Avior, we help families work through the full picture of inherited accounts: identifying the applicable rules, modeling distribution strategies across the 10-year window, and coordinating those decisions with the rest of a client’s tax and investment plan. If you or someone in your family is navigating an inherited IRA or retirement account this filing season, reach out to Avior to schedule a consultation and make sure the right decisions are made while time remains.

Investment management and financial planning services are offered through Avior Wealth Management, LLC, an SEC-registered investment adviser. Tax and accounting services are provided by Avior Tax and Accounting, LLC, a wholly-owned subsidiary of Avior Wealth Management, LLC.

Insurance products, including life, disability, long-term care, and annuities, are offered through Avior Insurance. Insurance and annuity products are not offered through Avior Wealth Management, LLC, and are not covered by SIPC. Avior Insurance operates independently to provide insurance solutions tailored to clients’ needs. Insurance products are subject to the terms and conditions of the issuing carrier.

All information contained herein is general in nature and is not to be construed as specific investment advice. Avior does not provide legal advice. Clients should consult their own legal, tax, and financial professionals before making any decisions. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results.

No Comments

Sorry, the comment form is closed at this time.