The Post-Appointment Action Plan: What to Do After You File

Hitting “submit” on your tax return feels like crossing a finish line. The forms are done, the receipts are organized, and you can finally stop thinking about W-2s and 1099s. Most people close their tax software and move on with their lives, assuming the work is complete.

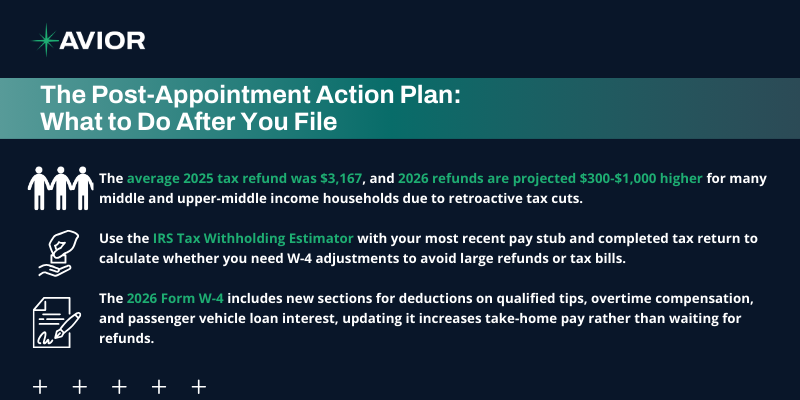

Filing your return triggers a new set of financial decisions that could save you thousands of dollars over the coming year. The average tax refund in 2025 was $3,167, and many filers in 2026 are projected to receive refunds $300 to $1,000 higher than typical thanks to retroactive tax cuts from the One Big Beautiful Bill. Whether you owed money or received a refund, your tax outcome reveals important information about your financial strategy going forward.

Key Takeaways

- The average 2025 tax refund was $3,167, and 2026 refunds are projected $300-$1,000 higher for many middle and upper-middle income households due to retroactive tax cuts.

- Use the IRS Tax Withholding Estimator with your most recent pay stub and completed tax return to calculate whether you need W-4 adjustments to avoid large refunds or tax bills.

- The 2026 Form W-4 includes new sections for deductions on qualified tips, overtime compensation, and passenger vehicle loan interest, updating it increases take-home pay rather than waiting for refunds.

- Safe harbor rule: Pay at least 90% of current year’s tax or 100% of prior year’s tax (110% if income exceeds certain thresholds) to avoid underpayment penalties when you owe at filing.

- Strategic refund uses: Direct funds toward emergency reserves (3-6 months expenses), high-interest debt repayment (credit cards charging 18-25% APR), or IRA contributions for the prior tax year (deadline is April filing date).

- File amended returns using Form 1040-X within three years of the original filing date or two years of paying the tax to claim overlooked deductions from One Big Beautiful Bill provisions.

Why Post-Filing Action Matters

Most people treat tax filing as the end of their annual tax obligation. The days and weeks following your filing actually present the best opportunity to optimize your tax situation for the coming year.

Your Tax Outcome Reveals Planning Gaps

Large refunds or unexpected tax bills both signal misalignment between your withholding and actual tax liability. A $3,000 refund means you gave the government $250 per month interest-free when you could have invested that money, paid down debt, or used it for other financial goals. Owing $2,000 at filing suggests insufficient withholding that might have triggered underpayment penalties.

Your completed return provides the exact information needed to fix these issues for next year. You know your actual income, deductions, and credits rather than estimating. This precision enables accurate withholding adjustments.

Review and Adjust Your Withholding

Your first post-filing action should be evaluating whether your withholding matches your actual tax liability.

Calculate the Right Withholding Amount

The IRS Tax Withholding Estimator helps you calculate the right withholding amount for your situation. Gather your most recent pay stub, your completed tax return, and information about any side income or investment earnings. The tool walks through your expected income, deductions, and credits to recommend adjustments to your W-4.

This calculation accounts for recent tax law changes affecting 2025 and 2026 returns. The One Big Beautiful Bill introduced several provisions, deductions for tip income, overtime compensation, and enhanced deductions for seniors, that affect how much you should withhold going forward.

Understanding the New 2026 Form W-4

The 2026 Form W-4 includes new sections allowing employees to account for deductions on qualified tips, overtime compensation, and passenger vehicle loan interest stemming from recent tax law changes. If you receive tip income or work overtime regularly, updating your W-4 to reflect these deductions increases your take-home pay throughout the year rather than waiting for a refund.

Submit your updated W-4 to your employer’s payroll department. Changes typically take effect within one to two pay periods. If you hold multiple jobs, complete the Two-Earners/Multiple Jobs worksheet to avoid under-withholding. Married couples where both spouses work should coordinate their withholding to prevent surprises at next year’s filing.

If You Received a Large Refund

Large refunds signal over-withholding throughout the year. While getting money back feels rewarding, that cash could have worked for you during the preceding twelve months.

Calculate the True Cost

Calculate what your refund represents on a monthly basis. Hypothetically, a $3,000 refund equals $250 per month you could have invested, saved, or used to pay down debt. If you had invested that $250 monthly in a portfolio earning 7% annually, you would have accumulated roughly $3,100 by year-end instead of the flat $3,000 refund. That’s $100 in lost opportunity cost from a single year of over-withholding.

Over a decade, this pattern costs thousands in foregone investment returns. The compounding effect of having that money available throughout each year rather than locked up until refund time adds up substantially.

Adjust Withholding to Optimize Cash Flow

Consider adjusting your withholding to bring your refund closer to zero while avoiding an amount owed. Some people prefer modest refunds as forced savings, which works fine if that strategy aligns with your goals. Just recognize the trade-off between convenience and opportunity cost.

The ideal target is a small refund or small balance due, perhaps $200-500 either way. This range indicates accurate withholding while providing a margin of error that prevents penalties if your situation changes slightly during the year.

If You Owed Money at Filing

Owing at tax time might indicate insufficient withholding, substantial investment income, or side business earnings without proper estimated payments.

Understand Underpayment Penalties

Review whether you made quarterly estimated tax payments if you’re self-employed or have significant non-wage income. The IRS charges underpayment penalties when you don’t pay enough tax throughout the year.

Generally, you must pay at least 90% of the current year’s tax or 100% of the prior year’s tax (110% if your income exceeds certain thresholds) to avoid penalties. The safe harbor of paying 100% of prior year tax provides certainty even when current year income increases unexpectedly. Adjusting your withholding or increasing estimated payments prevents this issue next year.

Set Up Estimated Payment Systems

If you’re self-employed or have significant investment income, set up a system for quarterly estimated tax payments. Missing estimated payment deadlines triggers penalties even if you ultimately receive a refund. Calendar reminders for the four quarterly due dates (April 15, June 15, September 15, and January 15) help ensure timely payments.

Consider setting aside a percentage of each payment or distribution you receive throughout the quarter. This approach smooths cash flow by accumulating tax reserves gradually rather than facing large quarterly payment obligations all at once.

Strategic Uses for Tax Refunds

Projected refunds for 2026 are expected to increase by $300 to $1,000 for many middle and upper-middle income households due to retroactive tax cuts. This windfall presents opportunities to strengthen your financial position rather than letting the money disappear into general spending.

Build Emergency Reserves First

An emergency fund covering three to six months of expenses provides critical protection against job loss, medical bills, or unexpected repairs. If your emergency fund falls short of this target, direct your refund there first.

High-yield savings accounts currently offer competitive interest rates, allowing your emergency reserves to earn returns while remaining accessible. This beats the zero return you earned while the government held your over-withheld funds. Building adequate reserves also prevents you from tapping retirement accounts or credit cards during emergencies, moves that carry penalties and high interest costs.

Eliminate High-Interest Debt

High-interest debt, particularly credit cards charging 18% to 25% APR, destroys wealth faster than almost any investment can build it. Applying your refund to credit card balances, personal loans, or car payments generates a guaranteed return equal to the interest rate you’re avoiding.

Paying off a credit card charging 20% interest provides an immediate 20% return on that money. No investment offers guaranteed 20% returns. This makes debt repayment one of the most powerful uses for refund dollars when you carry high-interest balances.

Boost Retirement Contributions

Tax refunds create an opportunity to boost retirement savings without impacting your regular cash flow. You can contribute to an IRA for the 2025 tax year until the April filing deadline in 2026, then adjust your ongoing contributions for 2026 based on your updated withholding.

This strategy works particularly well when your refund resulted from over-withholding. You’re essentially redirecting money that was already coming out of your paycheck, just routing it to retirement savings rather than tax overpayment. Then you adjust your W-4 to reclaim that cash flow going forward, allowing you to maintain or increase the retirement contribution level.

Consider Roth Versus Traditional Contributions

Consider whether Roth or traditional contributions make more sense for your situation. Roth contributions don’t reduce current taxable income, which might seem counterintuitive after just filing taxes. However, the tax-free growth and qualified withdrawals can provide substantial long-term benefits.

Traditional contributions reduce taxable income, providing immediate tax benefits. This works well if you’re currently in a higher tax bracket than you expect during retirement. Roth contributions work better if you’re in a lower bracket now or expect higher taxes in retirement.

Review Missed Deduction Opportunities

The One Big Beautiful Bill introduced several provisions affecting 2025 returns filed in 2026, including deductions for tip income, overtime compensation, car loan interest for certain vehicles, and enhanced deductions for seniors.

File Amended Returns for Overlooked Deductions

Review whether you qualify for any deductions you missed on your recently filed return. You can file an amended return using Form 1040-X if you discover errors or overlooked deductions. The IRS accepts amended returns within three years of the original filing date or within two years of paying the tax, whichever is later.

These changes sunset in 2028, creating a limited window to benefit from them. If you worked overtime in 2025 but didn’t claim the overtime deduction, filing an amended return could recover hundreds or thousands in overpaid taxes. The same applies to tip income deductions and enhanced senior deductions.

Update Your Strategy for Current Year

Update your tax planning strategy to capture these benefits for the current year. If you qualify for tip income or overtime deductions, ensure your W-4 reflects these so you get the benefit through increased take-home pay rather than waiting for next year’s refund.

Document these deductions carefully throughout the year. Keep records of tip income, overtime hours, and qualifying vehicle loan interest so you can substantiate these deductions when you file next year.

Build Systems for Next Year

Tax filing becomes less stressful when you maintain organized records throughout the year.

Create Document Organization Systems

Create a digital or physical folder system for tax documents as they arrive. Scan receipts for charitable contributions, business expenses, and medical costs immediately rather than scrambling to locate them next January. Cloud-based storage with mobile apps makes this process nearly effortless, photograph receipts when you receive them, and they’re automatically organized and backed up.

This ongoing organization also helps you track whether you’re on pace to exceed the standard deduction threshold for itemizing. If you’re close, you might bunch charitable contributions or medical expenses into one year to exceed the threshold and itemize, then take the standard deduction in alternate years.

Schedule Quarterly Tax Check-Ins

Set calendar reminders for quarterly tax check-ins even if you’re not required to make estimated payments. These check-ins let you review year-to-date income, assess whether your withholding remains accurate, and identify any tax planning opportunities before year-end eliminates them.

Quarterly reviews catch issues early when correction is easy. Discovering in December that you’ve under-withheld all year leaves limited options. Discovering in March or June provides time to increase withholding for the remaining months or make adjustments to income and deductions.

Work With Us

The actions you take in the weeks following tax filing can generate more value than the filing process itself. Adjusting your withholding to match your actual tax liability, strategically deploying refunds toward high-impact financial goals, and building systems to streamline next year’s process all compound over time. The retroactive tax cuts affecting 2025 returns create a unique opportunity for many households to receive larger refunds in 2026, making thoughtful planning around these funds especially important.

At Avior, we help clients integrate tax planning into their broader financial strategy throughout the year. Our team works with you to optimize withholding, coordinate tax-efficient investment strategies, and make informed decisions about refund deployment that align with your long-term goals. Contact us to discuss how we can help you move beyond reactive tax filing toward proactive tax planning that enhances your overall financial position.

No Comments

Sorry, the comment form is closed at this time.