AVIOR INSIGHTS – Why Wages Are Central to the Economic Outlook in 2023

Only one full week into 2023, news headlines have already sparked concern among some investors. From the protracted House Speaker battle in Congress to layoff announcements across industries, markets have been on edge. Despite these challenges, the pivotal issue continues to be whether the Fed will cause a recession in 2023, even if most economists believe it would be a shallow one. Slow or negative growth is already impacting profit forecasts across industries and could place further pressure on valuations. What should long-term investors be watching in order to focus on the big picture?

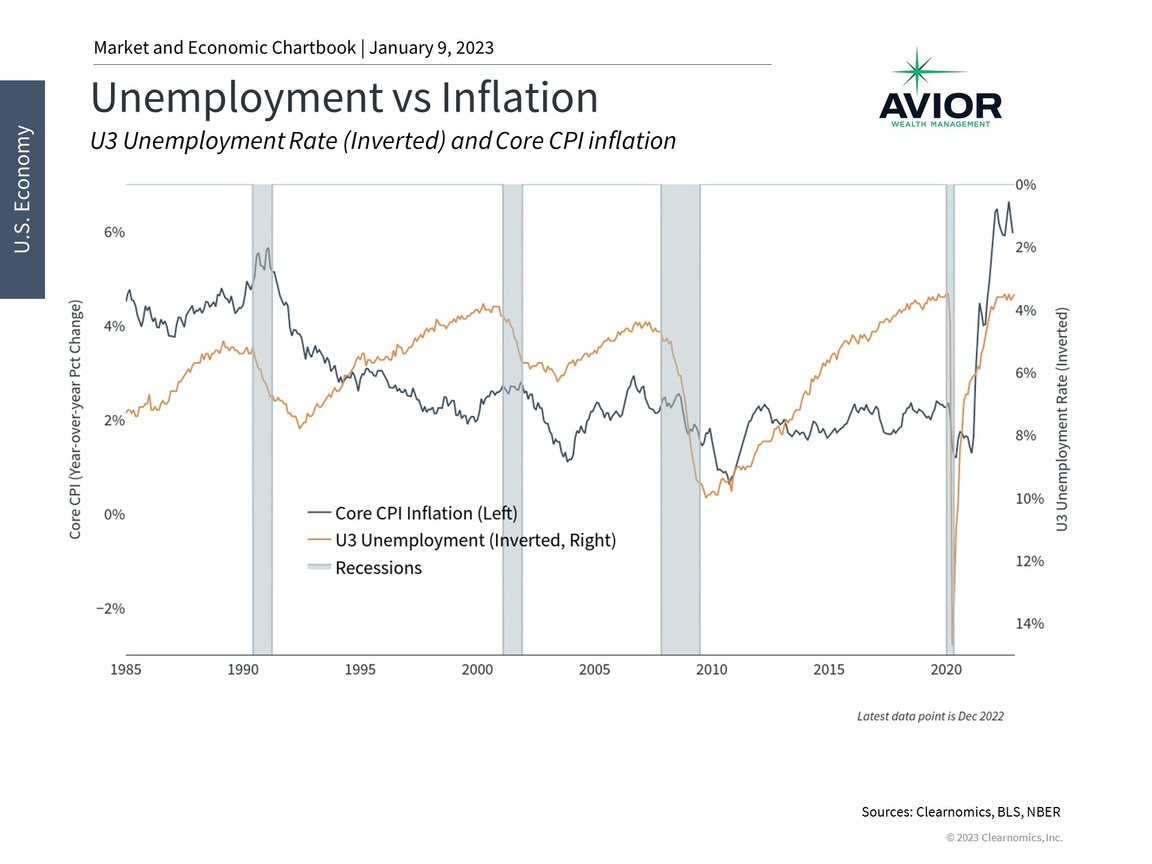

A tight labor market has historically contributed to higher inflation

The first jobs report of the year set the tone for this debate by showing that a healthy 223,000 jobs were added in December, bringing the unemployment rate down to only 3.5%, tying the lowest level since the 1960s. This means that the economy added 4.5 million net new jobs in 2022. While this doesn’t compare to the 6.7 million jobs created in 2021 as the economy bounced back from the pandemic, it is far above the 2.3 million and 2 million jobs added in 2018 and 2019, respectively. This is further evidence that the job market was strong last year despite negative GDP growth in the first half.

However, perhaps the more impactful data point for investors is the pace at which wages are rising. This is because wages and inflation are tightly linked. While higher pay for workers is certainly good news for households and individuals, markets often view this differently since wages that rise too quickly can spark “too much” consumer spending and spur inflation. Case in point: the surge in consumer demand during and after the pandemic was an important driver of the shortages and supply chain disruptions of the past few years.

Additionally, since wages represent costs to employers, upward pressure on pay results in inflation for businesses and corporations. As workers get paid more and businesses feel the pinch to profit margins, there may be stronger incentives to raise prices which in turn motivates workers to ask for even higher wages. This can result in a wage-price spiral that is difficult to reverse.

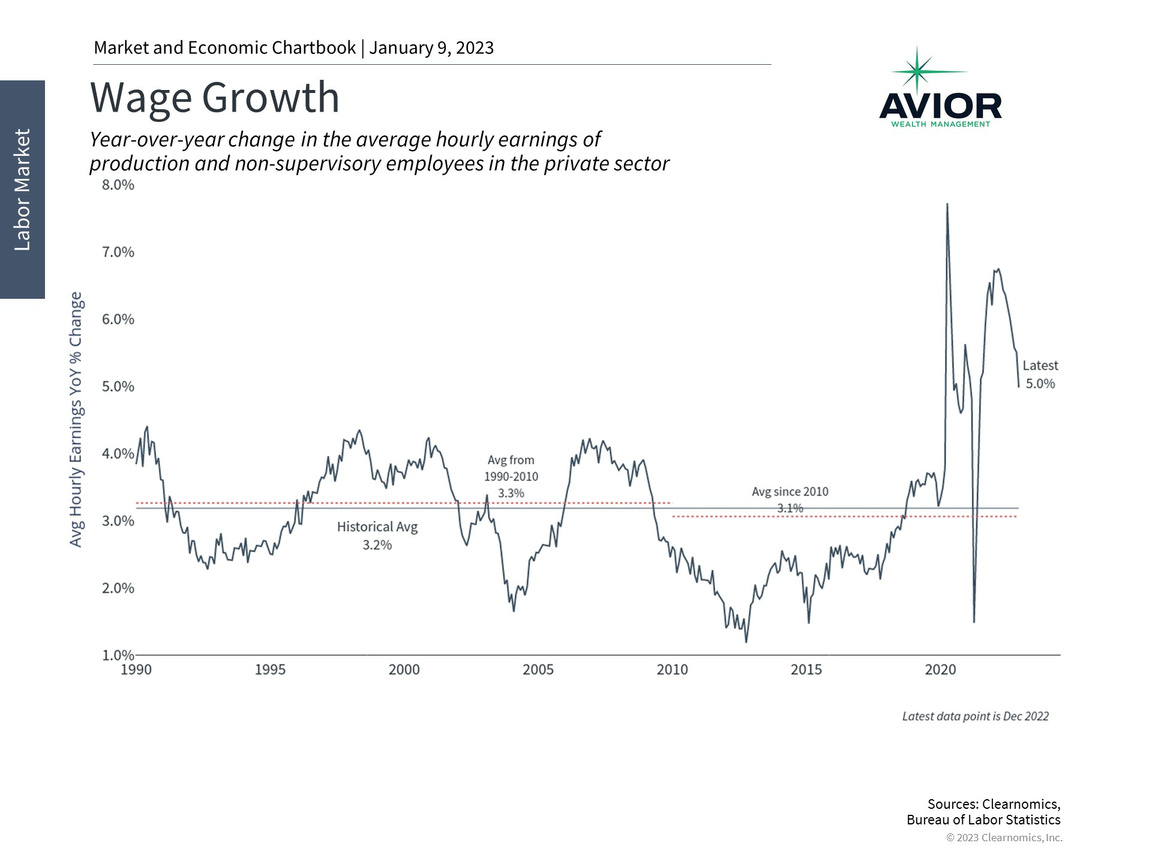

Wage gains are still strong but decelerating, a positive sign for inflation

So, the fact that wage gains slowed in December’s jobs report was taken as a positive sign by investors. Wage growth decelerated to 4.6% for the private sector and 5.0% for production and non-supervisory workers (i.e., those who tend to be paid hourly). This was better than economists had expected and represents a healthy deceleration from the 5.6% private sector peak last March. In many ways, this data is consistent with other slowdowns in inflation over the last few months from energy prices to shelter costs.

Other data show similar trends. The Employment Cost Index compiled by the Bureau of Labor Statistics suggests that salaries and wages decelerated from 5.7% last June to 5.2% in September. The Atlanta Fed Wage Tracker has also declined from a peak of 6.7% in July and August to 6.4% in November. While these moves may not seem large, they are all in the right direction.

The latest wage data led to an immediate market rally since lower wage pressures correspond to slowing inflation, and thus a slowing of Fed rate hikes. While positive, it’s important that investors not get ahead of themselves. After all, the numerous market swings last year were driven by market hopes that the Fed would begin to back off. In many cases, these hopes left investors disappointed when the Fed reiterated its commitment to keeping rates high.

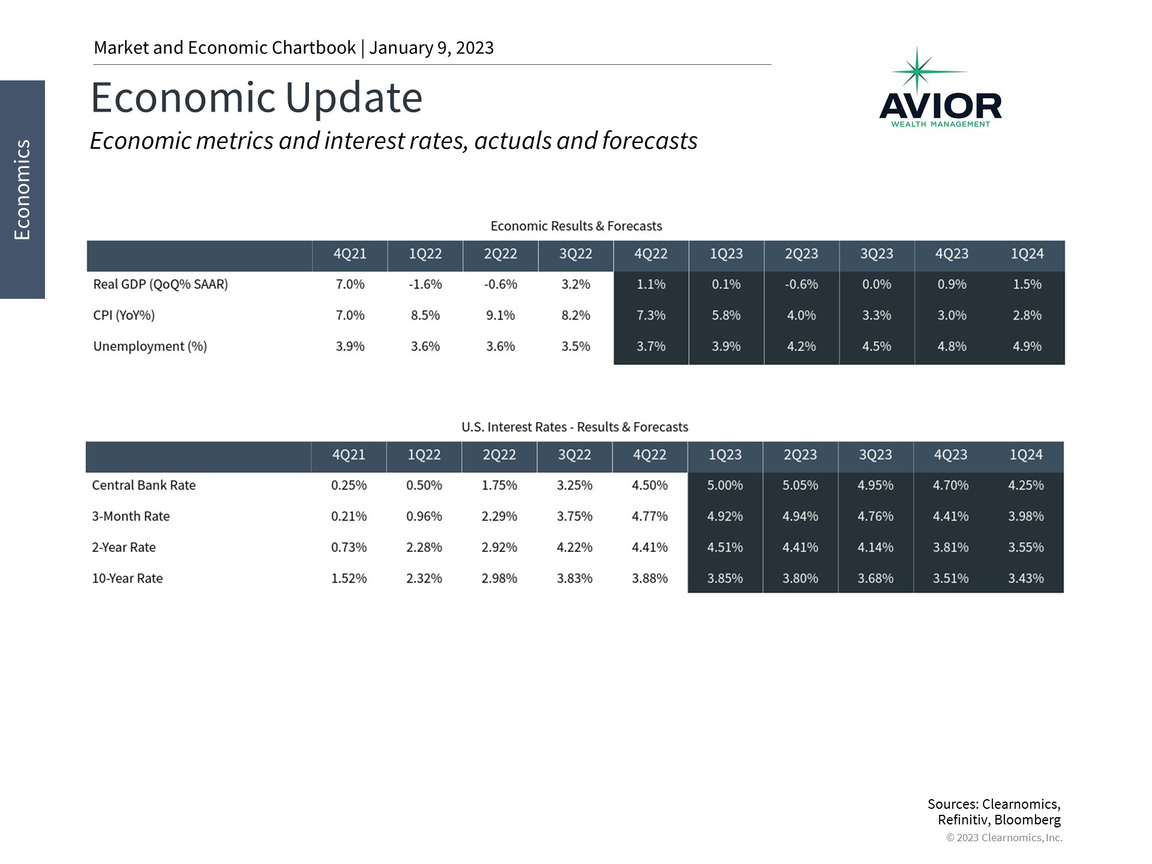

Economic forecasters expect minimal growth in 2023 due to Fed rate hikes

In light of this, current forecasts suggest that growth could be flat for the year, with GDP slightly negative in the second quarter and positive again in the fourth. These projections are very sensitive to the Fed, inflation and interest rates, just as they were last year, and could surprise to the upside if inflation does improve faster than expected and the Fed is convinced to take a pause. Until that happens though, investors ought to follow the long-term trends in these data and not get caught up in month-to-month moves.

The bottom line? Whether there will be a recession in 2023 is still the biggest question among market participants. Long-term investors should stay diversified and disciplined as this evolves over the next several months.

Disclosure: This report was obtained from Clearnomics, an unaffiliated third-party. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.avior.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments.

Avior Wealth Management, LLC, 14301 FNB Pkwy, Suite 110, Omaha, Nebraska 68154, United States, 402-218-4064

No Comments

Sorry, the comment form is closed at this time.