AVIOR INSIGHTS – How Investors Can Take Advantage of Attractive Valuations

First, it’s important to discuss why valuations matter. In short, valuation measures are the best tools that investors have to gauge the attractiveness of the stock market over years and decades. Unlike stock prices on their own, valuations don’t just tell you how much something costs, but tell you what you get for your money in terms of earnings, book value, cash flow, dividends, and other fundamental measures. After all, holding shares of a company means you are entitled to a portion of its profitability, so paying an appropriate price for this can improve the odds of future gains.

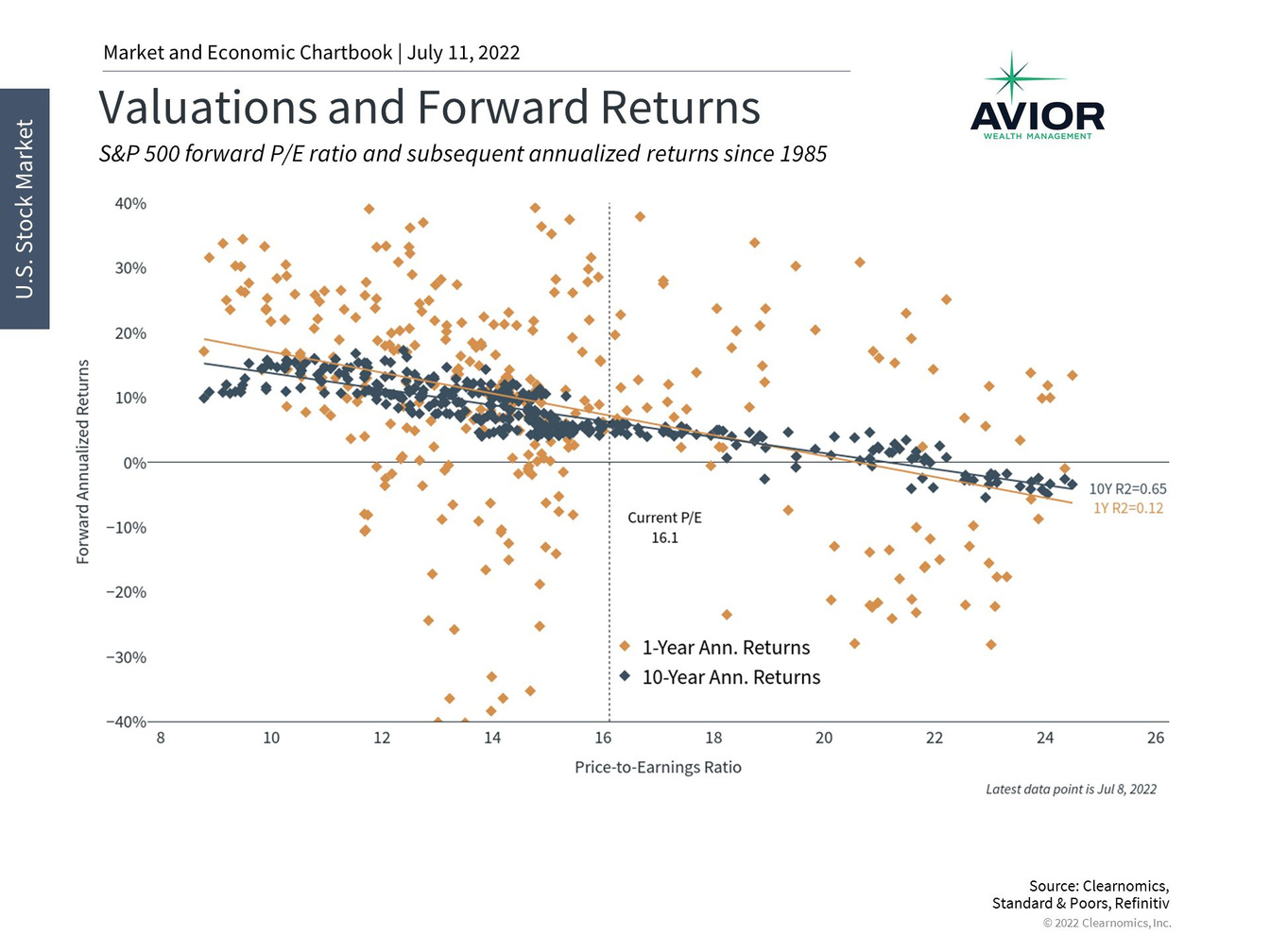

Valuations are highly correlated with long-run returns

Valuations are correlated with long-term portfolio returns for this reason – i.e., buying when the market is cheap improves the chances of success and vice versa. The chart above shows how the forward price-to-earnings ratio, which uses earnings estimates over the next twelve months, corresponds to subsequent 1-year and 10-year annualized returns. The dots for 10-year annualized returns cluster more tightly around the trend line than do 1-year returns which can vary significantly.

The fact that any metric is this highly correlated with stock market returns is quite amazing. To a large extent, the reason this pattern exists is exactly that it is difficult to stay invested when markets fall and valuations are the most attractive. Just think about how most investors feel today, or back in March 2020, or during 2008. Staying patient is much easier said than done, but this data emphasizes how important it is in order to achieve financial goals.

There are other reasons valuations are much better indicators than prices alone. Prices can rise over long periods of time, just as they have for the U.S. stock market over the past century, despite bear markets and short-term corrections. Comparing prices today to previous peaks and troughs doesn’t make much sense across these distinct time periods. Valuations, on the other hand, “normalize” prices by some important measure such as sales, earnings or cash flow, and can thus be a guide across different market cycles. This adjustment makes prices more comparable over time to determine whether an asset class, sector or individual investment is attractive.

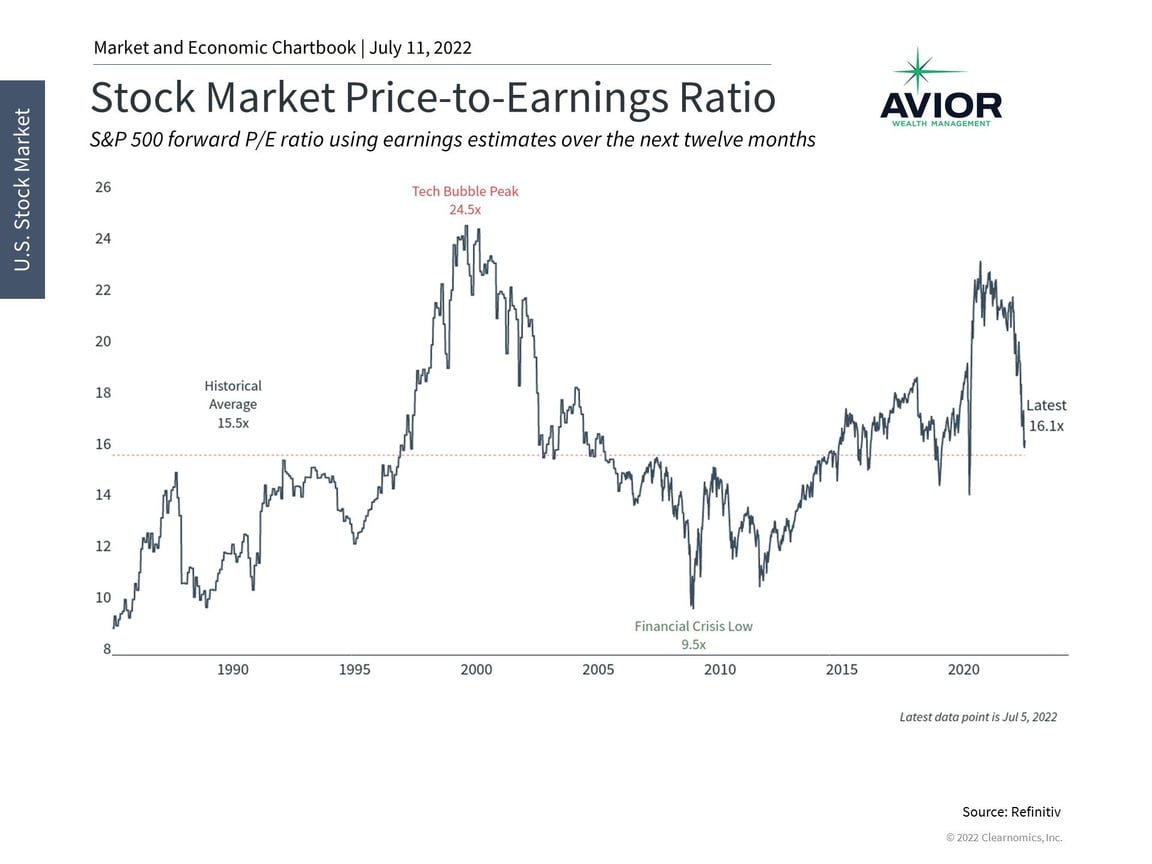

Today, various measures of value are far more attractive than they were even six months ago. As the chart below shows, the price-to-earnings ratio of the S&P 500 has fallen from near the peaks last seen during the dot-com bubble of the late 1990s and early 2000s, back toward the long run historical average. This closely-watched measure using next-twelve-month earnings estimates is hovering around 16.1x. Similarly, the Shiller P/E ratio, also known as the cyclically-adjusted P/E since it uses ten years of inflation-adjusted earnings, has declined to 28.9 from almost 39 at the end of 2021.

Stock market valuations are more attractive today

This same pattern can be found across a wide variety of valuation measures, from price-to-sales to dividend yields. Across asset classes, especially public equities, valuations are much more attractive today than at any point since mid-2020. Could valuations fluctuate further? Of course. If the market declines, valuation levels could look even more attractive. Conversely, if earnings decline as the economy decelerates, this could push valuations higher since lower profits mean that share prices are more expensive.

However, the point is that valuations are not a timing tool. As discussed above, valuations have very little historical correlation with returns over shorter time periods including one-year periods. It’s over several years or more that they begin to correspond to more attractive expected returns. For this reason, valuations are among the most important tools for constructing long run portfolios. This is true even though markets can continue to rise or fall regardless of valuations in the meantime.

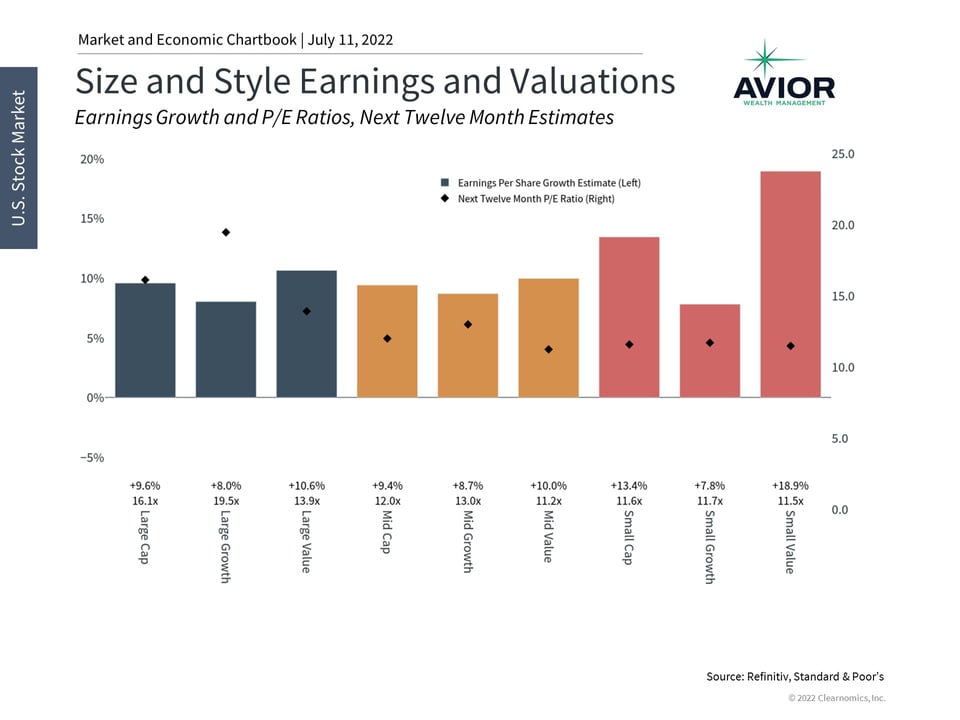

Different sizes, styles and sectors are more cheaply valued

Size and Styles Earning and Valuations Image

The bottom line? Where valuations go from here will be important for the direction of long run returns. However, investors should continue to stay invested and diversified as the cycle shifts from a bear market to an eventual recovery.

Disclosure: This report was obtained from Clearnomics, an unaffiliated third-party. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.avior.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange-traded funds, or any similar instruments.

Avior Wealth Management, LLC, 14301 FNB Pkwy, Suite 110, Omaha, Nebraska 68154, United States, 402-810-7831

No Comments

Sorry, the comment form is closed at this time.