The Hidden Benefits of Starting College Savings During the Holidays

The holidays bring plenty of traditions. You’ve got the cookie exchanges, the annual family gatherings, and the mountains of toys that end up forgotten by February. But buried under all those wrapping paper scraps is an opportunity most families overlook. While everyone else is buying the season’s hottest gadgets and trending toys, you could be setting up something that lasts far beyond the new year.

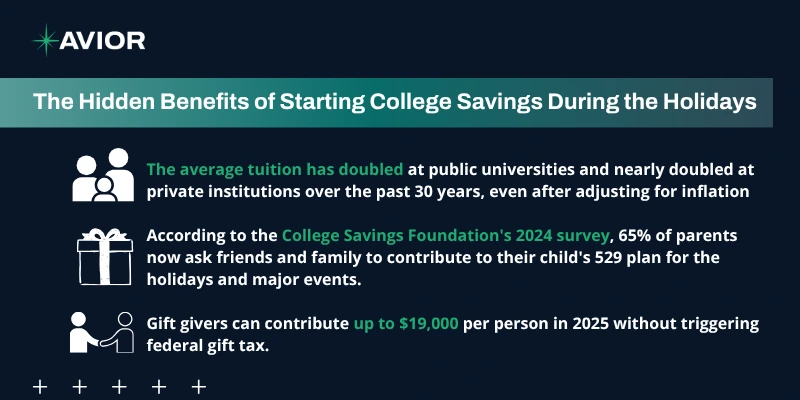

College costs keep climbing. The average tuition has doubled at public universities and nearly doubled at private institutions over the past 30 years, even after adjusting for inflation. Most families know they should save for education, but the holidays feel like the wrong time to think about it. Actually, this season offers unique advantages for starting or boosting college savings that you won’t find any other time of year. Let’s explore why December might be the smartest month to get serious about your child’s educational future.

The Gift-Giving Advantage

Something interesting has been happening with how families approach holiday presents. According to the College Savings Foundation’s 2024 survey, 65% of parents now ask friends and family to contribute to their child’s 529 plan for the holidays and major events. That’s up from just 45% in 2023.

Grandparents, aunts, uncles, and close friends want to give meaningful gifts. They just need permission to skip the toy aisle. When you open a 529 plan during the holidays, you create an immediate opportunity for others to contribute. Those $50 and $100 gifts from relatives might seem small, but they compound over years and can make a real difference in what you ultimately save.

How Gifting Actually Works

Most 529 plans now offer online gifting platforms. You get a unique code or link that you can share via text, email, or social media. Your family members visit the link, make their contribution, and get a digital certificate they can give your child. The money goes straight into the account without any checks to mail or account numbers to remember.

Gift givers can contribute up to $19,000 per person in 2025 without triggering federal gift tax. A married couple could gift $38,000 per beneficiary per year. Some states even offer tax deductions to anyone who contributes, not just the account owner, which makes these gifts even more attractive to extended family.

The Timing Creates Momentum

Starting anything new takes mental energy. You need to research options, fill out paperwork, and set up automatic transfers. The holidays provide built-in motivation that you won’t have in March or July. Family conversations naturally turn to children’s futures during gatherings. Questions about school and plans for the coming year come up over dinner tables.

This social context makes it easier to talk about college savings without it feeling forced or awkward. When you mention you’re setting up a 529 plan, relatives often volunteer to contribute on the spot. That instant positive feedback creates momentum that carries into the new year.

The New Year Effect

People make financial resolutions in January. They want to save more and spend smarter. But if you wait until January to start researching 529 plans, you’re competing with gym memberships, diet programs, and a dozen other self-improvement initiatives. Starting in December means your college savings plan is already running when January arrives. You’ve checked the box before most people even write their resolution list.

Tax Benefits Work in Your Favor

Most states offer tax deductions or credits for 529 contributions. Some states let you count contributions made through December 31st toward that year’s tax deduction. Others give you until April 15th of the following year, but getting it done early means one less thing to track during tax season.

The specific benefits vary by state. Colorado residents can deduct up to $25,400 per beneficiary (single) or $38,100 (joint) from state taxable income. Georgia allows married couples filing jointly to deduct up to $8,000 per beneficiary. Even if your state doesn’t offer deductions, the federal tax benefits still apply to everyone.

Long-Term Growth Starts Now

A 529 plan is an investment account. Your contributions go into mutual funds, ETFs, or age-based portfolios that grow over time. Starting in December instead of waiting until spring gives your money three or four extra months to compound. Over 18 years, that timing difference adds up.

The Flexibility You Might Not Know About

Recent legislation expanded how families can use 529 funds. You’re not locked into a traditional four-year college anymore. Starting in 2026, you can withdraw up to $20,000 per year tax-free for K-12 tuition. That’s double the previous limit. The funds now cover trade schools, apprenticeship programs, and certain continuing education costs too.

If your child doesn’t use all the money, you can roll up to $35,000 of unused funds into their Roth IRA starting in 2024, as long as the account has been open for at least 15 years. You can also change the beneficiary to another family member without penalty. This flexibility means starting a 529 carries less risk than many parents assume.

It Teaches Financial Values

Opening a college savings account during the holidays sends a message to your children about priorities. While they’re unwrapping presents, they learn that adults in their life are thinking about their future. Older children can understand when you explain that grandma’s smaller contribution might grow by the time they need it.

Some parents involve their kids in watching the account grow. They show them quarterly statements and explain how investing works. This turns the 529 into both a savings vehicle and an educational tool that teaches compound interest and long-term thinking.

Common Concerns Addressed

Many parents hesitate because they worry about making the wrong choice or committing to something they can’t maintain. You can start small. Most plans allow initial contributions as low as $25. You can adjust your monthly contributions based on your budget or pause them entirely if needed.

Choosing between plans feels overwhelming, but most financial advisors suggest your home state’s plan first since it often offers tax benefits. You’re not picking a college or locking your child into any specific path. You’re simply giving yourself options and time for the money to grow.

Work With Us

Starting a 529 plan during the holidays combines practical advantages with emotional momentum that makes the process easier than tackling it during any other season. The gift-giving culture creates natural opportunities for contributions, the timing helps with taxes, and the new year mindset supports building the savings habit. Small amounts contributed now have years to compound, and the expanded uses for these funds mean the money will serve your family regardless of which educational path your child ultimately chooses.

At Avior, we help families develop comprehensive education funding strategies that align with their overall financial goals. We can walk you through 529 plan options, explain the tax implications for your specific situation, and help you set up a sustainable savings approach that doesn’t strain your budget. If you’re ready to start your family’s college savings journey or want to optimize an existing plan, schedule a consultation with our team today. Let’s turn this holiday season into the moment you took control of your child’s educational future.

Investment management and financial planning services are offered through Avior Wealth Management, LLC, an SEC-registered investment adviser. Tax and accounting services are provided by Avior Tax and Accounting, LLC, a wholly-owned subsidiary of Avior Wealth Management, LLC.

Insurance products, including life, disability, long-term care, and annuities, are offered through Avior Insurance. Insurance and annuity products are not offered through Avior Wealth Management, LLC, and are not covered by SIPC. Avior Insurance operates independently to provide insurance solutions tailored to clients’ needs. Insurance products are subject to the terms and conditions of the issuing carrier.

All information contained herein is general in nature and is not to be construed as specific investment advice. Avior does not provide legal advice. Clients should consult their own legal, tax, and financial professionals before making any decisions. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results.

No Comments

Sorry, the comment form is closed at this time.