How to Give More (and Save on Taxes) With Charitable Contributions This Holiday Season

The holiday season brings out something special in people. Between Thanksgiving and New Year’s Eve, Americans open their wallets to support causes they care about. Last year, donors gave an estimated $3.6 billion on GivingTuesday alone, and December accounts for roughly 30% of annual charitable donations. The spirit of giving runs strong during these months, but many donors miss opportunities to maximize both their impact and their tax savings.

Understanding how to give strategically transforms charitable donations from simple gestures into powerful tools for change. The right approach lets you support more causes while potentially lowering your tax bill. Whether you’re planning to donate a few hundred dollars or several thousand, knowing the rules and strategies for charitable giving can help you make every dollar count. With year-end tax deadlines approaching, now is the perfect time to review how you can give generously while taking full advantage of available tax benefits.

Key Takeaways

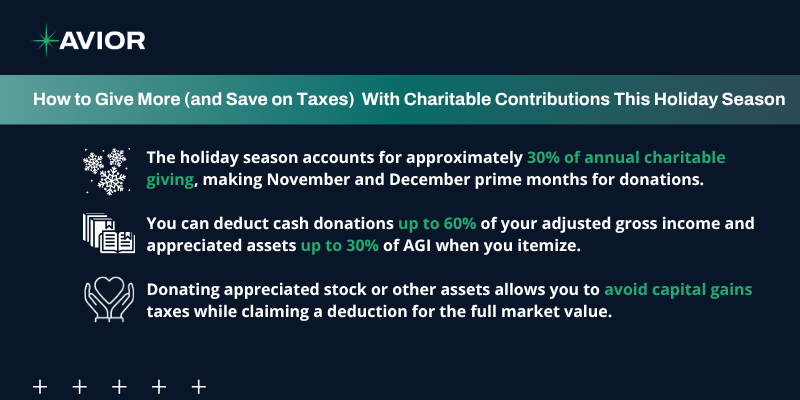

- The holiday season accounts for approximately 30% of annual charitable giving, making November and December prime months for donations.

- You can deduct cash donations up to 60% of your adjusted gross income and appreciated assets up to 30% of AGI when you itemize.

- Donating appreciated stock or other assets allows you to avoid capital gains taxes while claiming a deduction for the full market value.

- Qualified charitable distributions from IRAs let donors age 70½ and older give up to $108,000 tax-free in 2025.

- Bunching multiple years of donations into one year helps donors exceed the standard deduction threshold and maximize tax benefits.

- Working with a professional can help ensure your charitable strategy aligns with your overall financial plan and takes advantage of all available opportunities.

Why the Holiday Season Is Prime Time for Giving

The weeks between Thanksgiving and New Year’s Eve create a perfect environment for charitable giving. Multiple factors drive this surge in generosity beyond just holiday spirit.

Tax Deadlines Create Urgency

Donations must be completed by December 31st to count toward the current year’s tax return. This hard deadline prompts many people to finalize their charitable plans before the year ends. Those who want to claim deductions for the current tax year need to act during the holiday season.

Year-End Bonuses and Financial Reviews

Many people receive year-end bonuses, making December an ideal time to give. Additionally, individuals often review their annual finances during this period, discovering opportunities to reduce taxable income through charitable contributions. The combination of available cash and tax awareness creates momentum for donations.

Understanding Current Tax Rules for Charitable Giving

Tax laws governing charitable donations can feel complex, but understanding the basics helps you make informed decisions about your giving strategy.

Itemizing vs. Taking the Standard Deduction

To deduct charitable contributions on your taxes, you must itemize deductions on Schedule A of your tax return. For 2025, the standard deduction is $15,750 for single filers and $31,500 for married couples filing jointly. Your itemized deductions must exceed these amounts for itemizing to make financial sense.

Approximately 90% of taxpayers now take the standard deduction because it’s higher than their total itemized deductions. This doesn’t mean charitable giving lacks value, but it does mean most people won’t receive a direct tax benefit unless they employ strategic approaches.

Deduction Limits You Need to Know

The IRS limits how much you can deduct based on the type of donation and your adjusted gross income. Cash contributions to public charities can be deducted up to 60% of your AGI. Donations of appreciated assets like stock, real estate, or mutual funds have a lower limit of 30% of AGI.

If your donations exceed these limits, you can carry forward the excess for up to five years. This carryforward provision helps ensure you don’t lose the tax benefit of large donations.

Smart Strategies for Maximizing Your Charitable Impact

Strategic giving approaches help you support more causes while optimizing tax benefits. These methods work particularly well during the holiday season when charitable giving is top of mind.

Donate Appreciated Assets Instead of Cash

When you sell stocks or other investments that have increased in value, you owe capital gains tax on the profit. However, when you donate those appreciated assets directly to a qualified charity, you avoid paying capital gains tax entirely. Plus, you can deduct the full market value of the asset.

Consider this hypothetical example: You own stock worth $10,000 that you purchased for $4,000. If you sell the stock and donate the proceeds, you’ll owe capital gains tax on the $6,000 profit. At a hypothetical 15% capital gains rate, that’s $900 in taxes, leaving you with $9,100 to donate. If you donate the stock directly, the charity receives the full $10,000, and you claim a $10,000 deduction.

Use Bunching to Overcome the Standard Deduction

Bunching involves concentrating multiple years of donations into a single year. This strategy helps you exceed the standard deduction threshold and itemize, then take the standard deduction in other years.

For instance, if you typically donate $8,000 annually, that amount won’t exceed the $15,750 standard deduction for single filers. But if you donate $24,000 in one year (three years’ worth), you can itemize and receive the tax benefit, then take the standard deduction the next two years. A donor-advised fund works well for bunching because you can contribute a large amount in one year, receive the immediate tax deduction, and distribute grants to charities over time.

Consider Qualified Charitable Distributions from IRAs

If you’re 70½ or older, qualified charitable distributions (QCDs) offer a tax-efficient way to give. You can direct up to $108,000 per year from your IRA directly to qualified charities. The distribution doesn’t count as taxable income, and it satisfies your required minimum distribution for the year.

QCDs work especially well for donors who don’t itemize deductions because the tax benefit comes from excluding the distribution from income rather than through a deduction.

Donor-Advised Funds: A Flexible Giving Vehicle

Donor-advised funds (DAFs) have become increasingly popular tools for charitable giving. These accounts function like charitable investment accounts, offering both tax benefits and flexibility.

How Donor-Advised Funds Work

You contribute cash, stock, or other assets to a donor-advised fund and receive an immediate tax deduction for the full amount contributed. The funds are invested and can grow tax-free. You then recommend grants to qualified charities whenever you choose.

This structure offers several advantages. You receive the tax deduction in the year you contribute, even if you distribute the funds to charities over several years. The investment growth means you can potentially give more than you initially contributed. And you have time to research and select the charities that best match your values.

Strategic Uses for DAFs

Donor-advised funds work particularly well for the bunching strategy mentioned earlier. You can contribute a large amount during a high-income year, receive the tax deduction, and then distribute the funds to your favorite charities over multiple years.

They’re also useful for managing volatile income. If you have a year with unexpectedly high earnings, you can contribute to a DAF to reduce your tax bill, then maintain your regular giving pattern from the fund.

Ensuring Your Donations Qualify for Deductions

Not all donations qualify for tax deductions. Knowing which organizations and types of contributions are eligible prevents disappointment at tax time.

Qualified Organizations

Only donations to IRS-recognized 501(c)(3) organizations qualify for deductions. These include churches, educational institutions, hospitals, and most charitable nonprofits. Political organizations, campaigns, and certain social clubs don’t qualify.

The IRS provides a Tax Exempt Organization Search tool where you can verify an organization’s status before donating. Taking this simple step helps ensure your donation will be deductible if you itemize.

Documentation Requirements

Keep detailed records of all donations. For cash donations under $250, a bank record or written communication from the charity works. For donations of $250 or more, you need a written acknowledgment from the organization stating the amount and whether you received anything in return.

Donations of property worth more than $500 require Form 8283. For property worth more than $5,000, you’ll need a qualified appraisal. These documentation requirements become more stringent as donation amounts increase.

Timing Your Donations for Maximum Impact

When you make donations matters as much as how much you give. Strategic timing can enhance both your charitable impact and tax benefits.

December 31st Is Your Hard Deadline

Donations must be completed by December 31st to count for the current tax year. For checks, the date you mail them counts. For credit card donations, the date you charge the card determines the tax year, not when your credit card bill is due.

Stock donations require more lead time. Transfers can take several days to complete, so don’t wait until the last week of December to initiate a stock donation. Many brokerages get overwhelmed with year-end transfers and may not process them in time.

Consider Giving Earlier in the Season

While December receives the most attention, giving earlier in November or even October offers advantages. Charities appreciate donations that arrive before their busiest season, giving them time to plan and use the funds effectively. You also avoid the year-end rush at brokerages and donor-advised fund sponsors.

Common Mistakes to Avoid

Even well-intentioned donors make errors that reduce the tax benefits of their charitable giving. Being aware of these common pitfalls helps you avoid them.

Missing Documentation

The most common mistake is failing to get proper documentation for donations. Without receipts or acknowledgment letters, you can’t prove your donations if the IRS questions them. Request acknowledgment letters immediately after making significant donations, especially in December when charities are busy.

Donating to Non-Qualified Organizations

Some worthy causes don’t qualify as 501(c)(3) organizations. GoFundMe campaigns for individuals, political donations, and contributions to some social clubs won’t provide tax deductions. Verify an organization’s status before expecting a tax benefit.

Selling Assets Before Donating

When you sell appreciated assets and donate the cash proceeds, you create an unnecessary tax bill. The capital gains tax reduces the amount available for charity and doesn’t provide additional tax benefits. Always donate appreciated assets directly to charity when possible.

Work With Us

Strategic charitable giving during the holiday season allows you to maximize both your philanthropic impact and tax savings. By understanding deduction limits, donating appreciated assets, using tools like donor-advised funds, and timing your contributions effectively, you can support more causes while reducing your tax burden. The key is planning ahead and better aligning your donations with both your charitable goals and overall financial strategy. As year-end approaches, taking time to review your giving plan helps you avoid valuable opportunities to make a difference.

At Avior, we help clients integrate charitable giving into their comprehensive financial plans. Our advisors can guide you through strategies like bunching donations, contributing appreciated assets, and using donor-advised funds to maximize tax benefits while supporting the causes you care about. We work with you to help align your charitable giving with your retirement planning, tax strategy, and legacy goals. Contact Avior today to schedule a consultation and discover how thoughtful charitable planning can help you give more effectively while building the financial future you want.

Investment management and financial planning services are offered through Avior Wealth Management, LLC, an SEC-registered investment adviser. Tax and accounting services are provided by Avior Tax and Accounting, LLC, a wholly-owned subsidiary of Avior Wealth Management, LLC.

Insurance products, including life, disability, long-term care, and annuities, are offered through Avior Insurance. Insurance and annuity products are not offered through Avior Wealth Management, LLC, and are not covered by SIPC. Avior Insurance operates independently to provide insurance solutions tailored to clients’ needs. Insurance products are subject to the terms and conditions of the issuing carrier.

All information contained herein is general in nature and is not to be construed as specific investment advice. Avior does not provide legal advice. Clients should consult their own legal, tax, and financial professionals before making any decisions. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results.

No Comments

Sorry, the comment form is closed at this time.