How Dollar-Cost Averaging Can Help Investors Get Into the Market

As with many things in life, knowing what we’re supposed to do and actually doing it are two separate things. This is true for our health, relationships, careers, and of course, our finances. When it comes to investing, it’s well known that properly diversifying and staying invested are the best ways to achieve long-term financial goals. However, this is often easier said than done, especially when market and economic outlooks are uncertain, as they have been for many years. Fortunately, there are investment methods for managing the emotions that come from market volatility. What should investors know about how they can stick to an investment plan through years and decades?

Dollar-cost averaging and lump sum investing

Knowing when and how to invest in the stock market can be challenging, especially if you suddenly come into a large sum of money through an annual bonus, the sale of a business, an inheritance, etc. In the long run, investing properly can turn savings into wealth. In the short run, however, market volatility can derail even the most steadfast investors.

This is where dollar-cost averaging can help. With dollar-cost averaging, investors regularly invest a set amount on a pre-planned schedule. This reduces the temptation to follow and react to every market move or to try to time the market. If you already make regular, automatic contributions to your portfolio with each paycheck, such as through a 401(k) plan at work, you are technically already using dollar-cost averaging. Whether these investments occur monthly, quarterly, or annually turns out to matter much less than simply sticking to a plan.

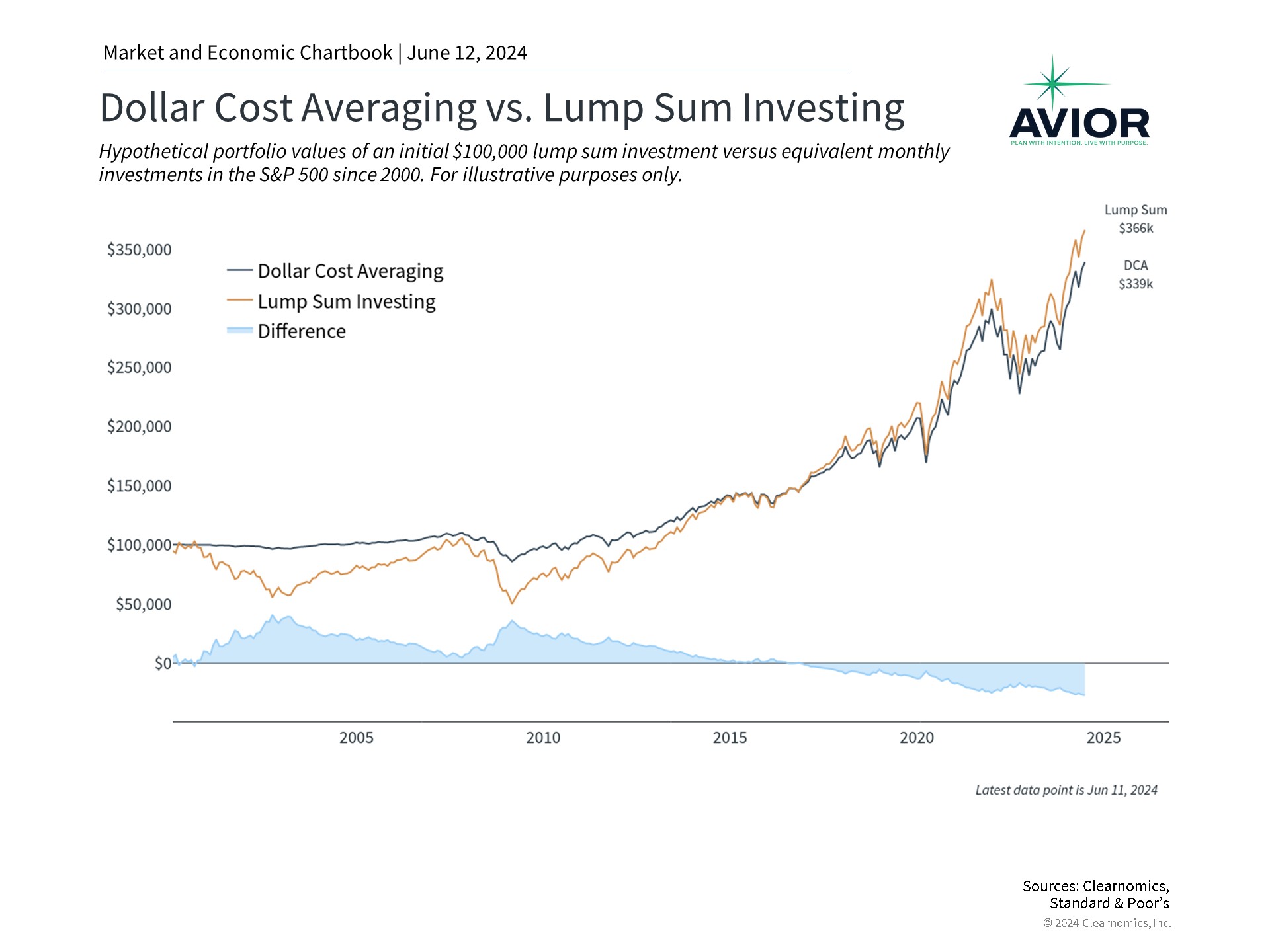

The opposite, investing all at once, is often known as lump sum investing. How your portfolio performs in the short run is very much determined by how the market performs immediately after the investment.

This can be seen in the chart above which shows the hypothetical returns between these two methods beginning in 2000. Investing $100,000 in the S&P 500 would have lost value almost immediately due to the dot-com crash. This would have recovered over the next several years until the housing crash. Finally, the value of this investment would have recovered in 2013 when the S&P 500 returned to all-time highs and then benefited from the long bull market that followed.

This chart also shows the hypothetical returns of a dollar-cost averaging approach in which the investor splits up the $100,000 into monthly investments over this full period. This is a rather extreme example given the length of the time period but it serves to highlight some key facts.

Dollar-cost averaging on a monthly schedule would have avoided the market drawdowns early in the period when the portfolio would have mostly been held in cash, remaining relatively flat through the mid-2010s. There is an inflection after this when the lump sum portfolio catches up and outperforms due to the strong bull market. So, both methods had their benefits and time to shine over the past two-and-a-half decades.

Dollar-cost averaging can make it psychologically easier to invest

The takeaway here is less about how to maximize returns than how to stay invested through years and decades. Dollar-cost averaging can help reduce risk in situations where markets fall sharply, especially early on. However, lump sum investing tends to outperform dollar-cost averaging in the long run since, historically, markets have steadily risen over time.

This is analogous to comparing a 100% stock portfolio to a properly diversified one that holds a balanced mix of stocks, bonds, and other asset classes. The 100% stock portfolio might outperform over long periods, especially during strong bull markets like today’s, but it will also experience sharper pullbacks. The diversified portfolio, on the other hand, will experience steadier growth and more muted declines, making it easier for investors to stay level headed.

This is especially relevant today with the market near all-time highs. The truth of the matter is that markets are always uncertain. Whether it’s the upcoming presidential election, geopolitical conflict, or the direction of interest rates and the economy, investors may worry that the market could pull back just after they invest.

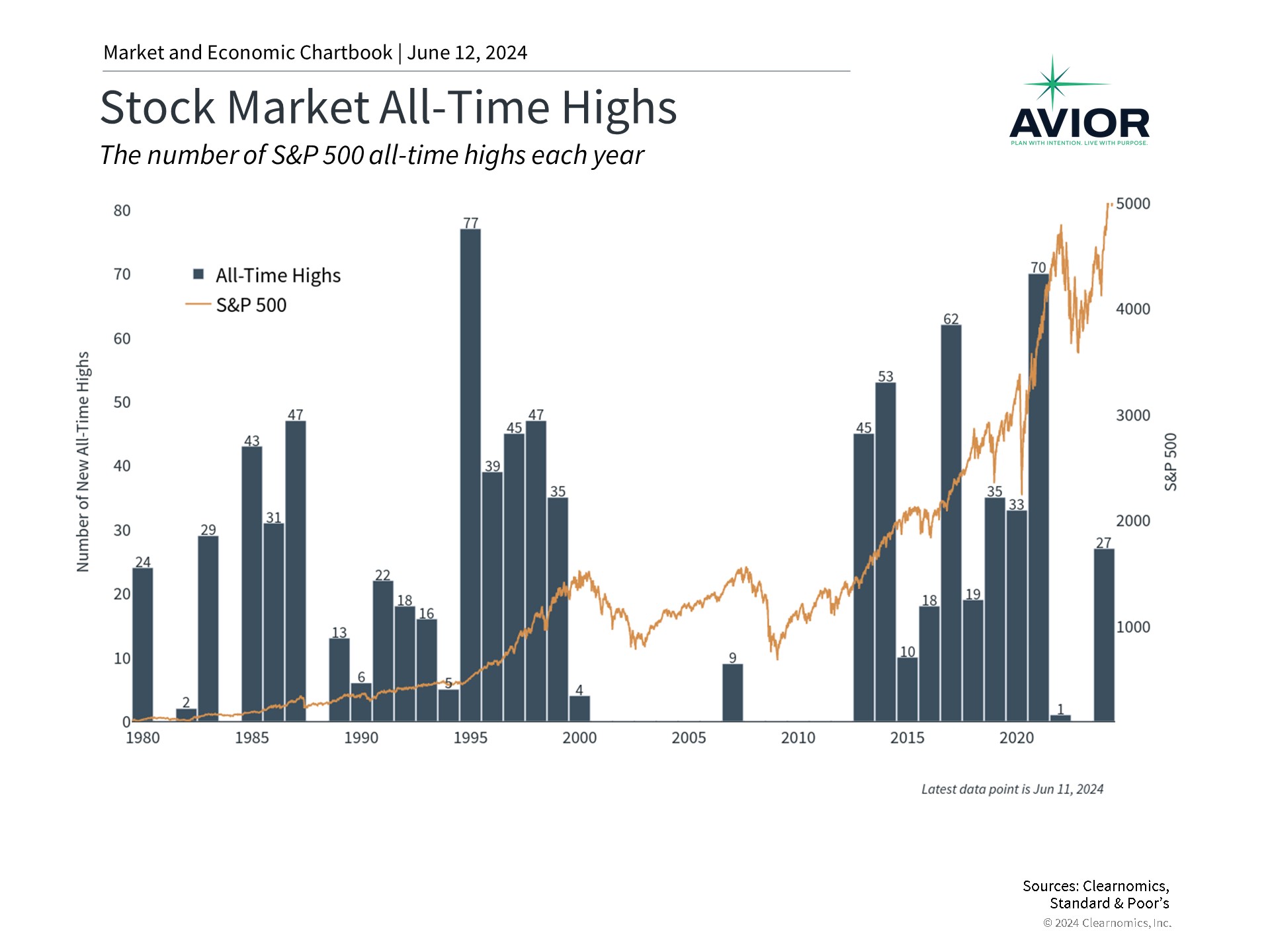

It’s important to keep in mind that just because the market is near a current peak doesn’t necessarily mean it’s “due for a pullback.” By definition, markets achieve many new all-time highs as they rise during bull markets. While there has been significant uncertainty this year due to interest rates, inflation, and the Fed, the S&P 500 has already experienced 24 new all-time highs. This includes a sharp rally in May after a slump in April.

Ironically, it can be psychologically difficult to invest both when the market is rising and when it is falling, for fear that the market might be at its peak in the first case, and that it might fall further in the second. So, whether dollar-cost averaging or lump sum investing makes more sense depends on the individual investor, their ability to handle risk, and their time horizon.

Getting invested sooner is better than waiting for the right timing

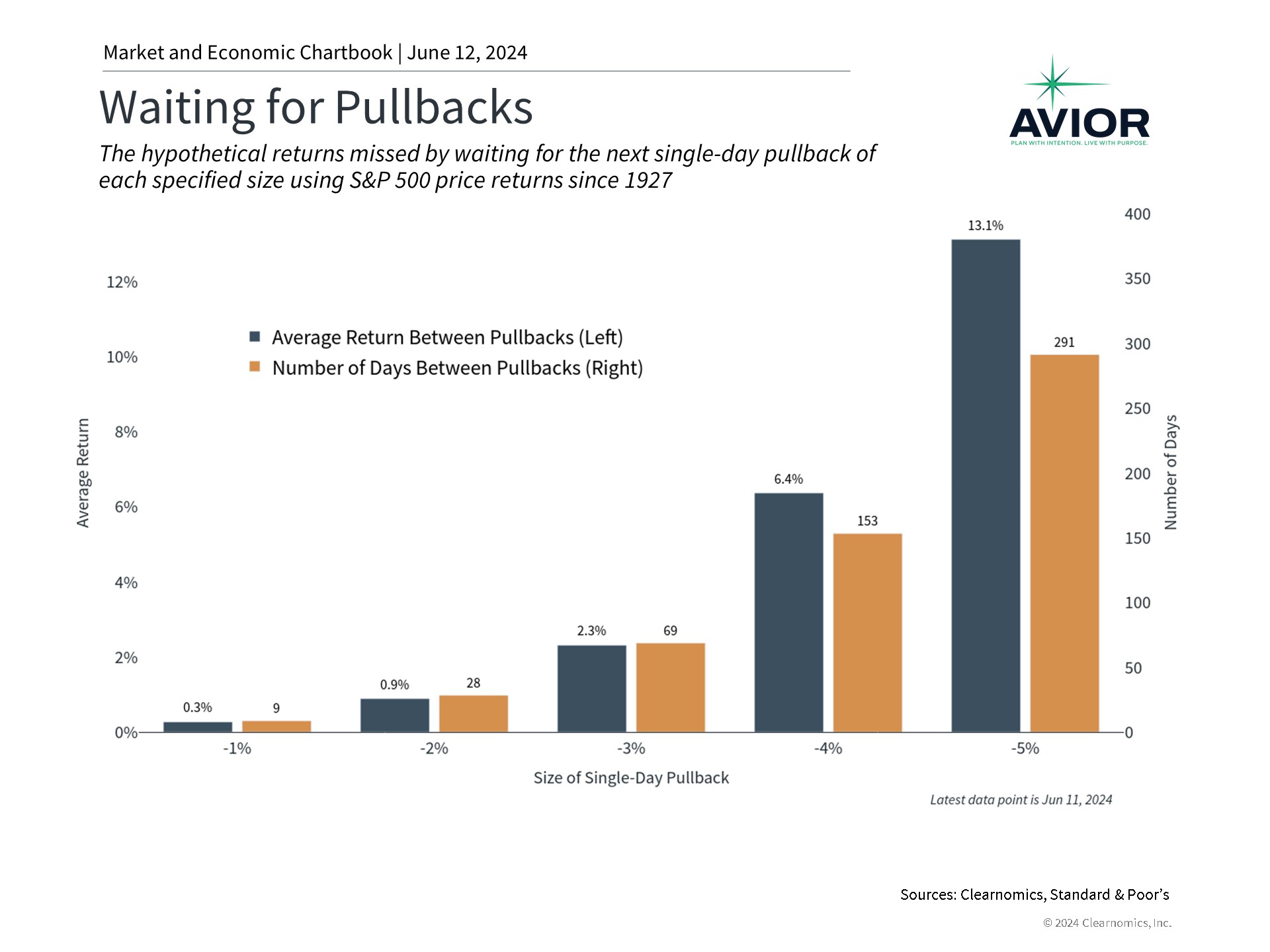

Whether you choose to dollar-cost average or invest all at once, getting into the market sooner has historically been better than “waiting for a pullback.” As the accompanying chart shows, waiting for a better time to buy or trying to “buy the dip,” has tended to backfire. Since the market tends to rise over time and can rebound unexpectedly, even the worst timing is often better than being out of the market.

For example, an investor waiting for a 5% pullback before investing would, on average, have waited 291 days. Even though 5% or worse pullbacks do occur periodically, the fact that the market rises over time means that there are often “higher lows” – i.e., the next dip is higher than before. Historically, markets have gained a whopping 13% during these periods, a figure which includes the pullback itself.

Just as a diversified portfolio can help reduce overall risk and volatility, so can dollar-cost averaging when it comes to investing over time. Dollar-cost averaging may not be the mathematically optimal way to invest, since lump sum investing has tended to outperform over history. However, it can help investors to stay focused on the long run without worrying about every market event or trying to time the market perfectly. As is always the case, seeking the guidance of a trusted financial advisor is the best way to determine the approach that works best for your specific goals.

The bottom line? Dollar-cost averaging and lump sum investing are both ways to invest cash. History shows that getting invested sooner is the most important way to achieve long-term financial goals.

Disclosure: This report was obtained from Clearnomics, an unaffiliated third-party. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.aviorwealth.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. Please remember to contact Avior, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian. A copy of our current written disclosure Brochure and Form CRS (Customer Relationship Summary) discussing our advisory services and fees continues to remain available upon request or at www.avior.com.

No Comments

Sorry, the comment form is closed at this time.