Do You Know What Happens To Your Assets If You Don’t Have An Estate Plan?

Death isn’t something most of us want to think about, especially when we’re busy living our lives, building careers, and raising families. Yet avoiding the conversation about what happens to your assets when you die doesn’t make the inevitable disappear. Without an estate plan, you’re essentially letting the state government decide who gets your house, your savings, and even custody of your children.

The reality might seem harsh, but it’s simple – if you don’t make these decisions yourself, someone else will make them for you. State laws, not your personal wishes, will determine how your assets are distributed. Your loved ones will face unnecessary stress, expense, and delays while courts sort through your affairs. What should be a time for grieving becomes a complex legal process that could have been avoided with proper planning.

Key Takeaways

- Without an estate plan, state intestacy laws determine how your assets are distributed.

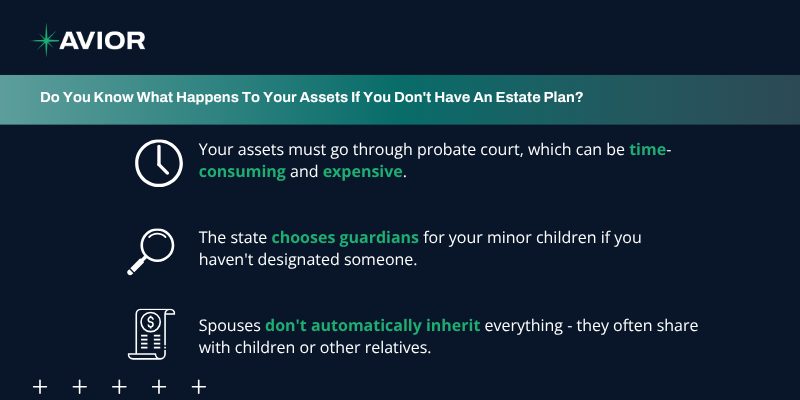

- Your assets must go through probate court, which can be time-consuming and expensive.

- The state chooses guardians for your minor children if you haven’t designated someone.

- Spouses don’t automatically inherit everything – they often share with children or other relatives.

- Joint accounts and beneficiary designations can bypass probate but have limitations.

- Creating an estate plan protects your family from unnecessary legal complications.

When the State Makes Your Decisions

If you die without a will or estate plan, you’ve died “intestate.” This legal term means the state where you lived will follow its intestacy laws to decide who inherits your property. These laws follow a strict hierarchy that starts with your closest relatives and works outward to more distant family members.

The state doesn’t consider your personal relationships, promises you made, or who actually needs the money most. It simply follows a formula. Your spouse might receive half your assets while your children get the other half, regardless of whether your spouse needs everything to maintain your home and lifestyle.

The Probate Process Takes Over

Without an estate plan, all your assets must go through probate court. This court-supervised process validates your debts, identifies your property, and distributes everything according to state law. Probate can take months or even years to complete, during which your family may struggle to access the resources they need.

The probate process is also public record. Details about your assets, debts, and family disputes become available for anyone to see. This lack of privacy can be embarrassing and may even make your family targets for scams or unwanted solicitation.

Your Children’s Future Probably Gets Decided by Strangers

If you have minor children and both parents die without naming guardians, the court will choose who raises them. While courts try to act in children’s best interests, they don’t know your family dynamics, values, or preferences. The person chosen might not share your beliefs about education, religion, or parenting styles.

The court will also control any inheritance your children receive until they reach adulthood. This means a court-appointed guardian will manage the money, making decisions about expenses for your children’s care, education, and needs.

Spouses Don’t Get Everything

One of the biggest misconceptions about dying without an estate plan is that your spouse automatically inherits everything. In reality, most states give spouses only a portion of the estate, with the rest going to children, parents, or siblings depending on your family situation.

If you have children from a previous relationship, your current spouse might receive even less. Some states give the spouse only a third of the estate, with the remainder split among all your children. This can create financial hardship for your surviving spouse and potential conflict between your spouse and children.

Assets That Bypass Probate

Not everything you own will go through probate. Some assets transfer automatically to designated beneficiaries or joint owners. Life insurance policies, retirement accounts, and bank accounts with named beneficiaries pass directly to those people without court involvement.

Property owned jointly with rights of survivorship also avoids probate. When one owner dies, the surviving owner automatically gets full ownership. This is common with married couples who own their home together.

The Costs Add Up

Probate isn’t free. Court fees, attorney costs, and administrative expenses can consume up to 10% of your estate’s value. Hypothetically, for a modest estate worth $200,000, this could mean $20,000 in fees that your family must pay before receiving any inheritance.

These costs come out of your estate before your family receives anything. The money you worked hard to save for your loved ones instead goes to lawyers and court systems. Simple estate planning documents could have avoided most of these expenses.

Family Conflicts Become Legal Battles

Without clear instructions about your wishes, family members may disagree about how to handle your affairs. These disputes often end up in court, where emotions run high and legal fees mount. Siblings might fight over who gets the family home, or step-children might challenge their step-parent’s right to inherit.

These conflicts can destroy family relationships permanently. What should be a time for families to support each other through grief becomes a source of lasting resentment and anger.

The Statistics You Should Be Aware Of

The numbers around estate planning are sobering. According to recent surveys, 67% of Americans don’t have a will, leaving their families vulnerable to all these problems. Many people assume they don’t have enough assets to worry about, but every adult has an estate that includes their possessions, accounts, and digital assets.

Even among those who recognize the importance of estate planning, only about 32% have actually created any documents. The gap between knowing you should plan and actually doing it often persists until it’s too late.

Simple Solutions Exist

Creating a basic estate plan doesn’t require vast wealth or complex legal strategies. A simple will can designate who gets your assets and who should care for your children. Adding beneficiary designations to your accounts can help those assets bypass probate entirely.

For many people, a revocable living trust offers even better protection. Assets in the trust avoid probate completely, maintaining privacy and allowing faster distribution to your beneficiaries. The trust can also provide instructions for managing your affairs if you become incapacitated.

Taking Action Before It’s Too Late

Estate planning isn’t just about death – it’s about protecting your family and maintaining control over your legacy. The longer you wait, the more likely it becomes that life circumstances will change, making your planning more complex or, in worst cases, impossible due to incapacity.

Starting with basic documents and updating them as your life changes helps your family stay protected. Even young adults with modest assets benefit from having a will, especially if they have children or specific wishes about their belongings.

Work With Us

The consequences of dying without an estate plan extend far beyond just distributing assets – they can fundamentally alter your family’s future and financial well-being. From court-appointed guardians raising your children to strangers making decisions about your life’s work, the lack of planning transfers control from you to the state. While these realities might seem overwhelming, they’re entirely preventable with proper planning.

At Avior Wealth Management, we understand that estate planning involves more than just legal documents – it’s about protecting your family’s future and preserving the legacy you’ve worked to build. Our comprehensive approach helps you coordinate your estate planning with your overall financial strategy, helping ensure your wealth transfer plans align with your investment goals and tax strategies. Contact us today to discuss how we can help you create an estate plan that protects your assets and provides financial confidence to you and your loved ones.

Investment advisory services provided by Avior Wealth Management, LLC (“Avior”), an SEC registered investment adviser for informational purposes only and should not be construed as financial, tax, or investment advice. The information presented reflects market conditions as of the date of this communication and is subject to change. Past performance is not indicative of future results. All investments involve risk, including the loss of principal.

While we strive for accuracy, Avior makes no representations as to the accuracy, completeness, or reliability of the information contained herein. You should consult with your financial advisor or tax professional to discuss your individual financial situation before making any investment decisions.

Market conditions and economic data may fluctuate, and future outcomes are uncertain. This newsletter does not guarantee future results and should not be relied upon as a sole basis for making any financial or investment decisions. Please consider your own risk tolerance and investment goals when evaluating strategies such as stock allocations.

No Comments

Sorry, the comment form is closed at this time.