Will vs. Trust: Which One Is Right for You?

You’ve been putting off estate planning for months, maybe years. Then suddenly life throws you a curveball – a health scare, a new grandchild, or maybe just watching the news about celebrity estate battles that turned families against each other. Now you’re ready to get your affairs in order, but you’re faced with a confusing choice: should you create a will or set up a trust?

The decision isn’t as straightforward as you might think. While both documents help ensure your assets reach the right people, they work in different ways and serve different purposes. Making the wrong choice could cost your family, expose your private affairs to public scrutiny, or leave your loved ones tied up in court for months. Understanding the key differences between wills and trusts is essential for creating an estate plan that truly protects your family’s future.

Key Takeaways

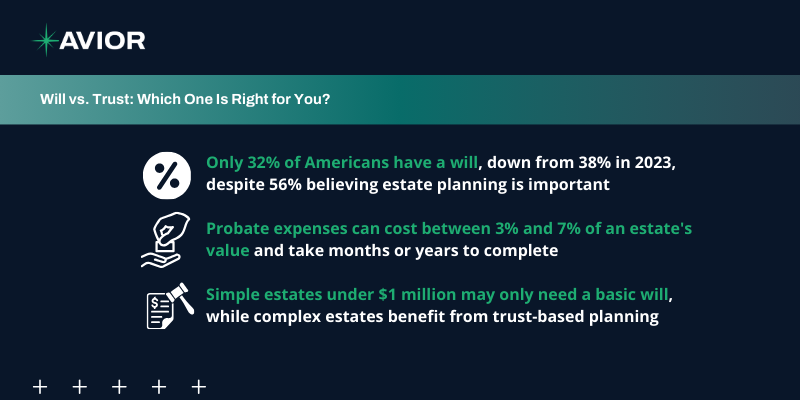

- Only 32% of Americans have a will, down from 38% in 2023, despite 56% believing estate planning is important

- Wills must go through probate court, while assets in properly funded trusts can bypass probate entirely

- Probate expenses can cost between 3% and 7% of an estate’s value and take months or years to complete

- Trusts provide privacy and immediate asset access, but cost more to set up and require ongoing management

- Most families benefit from having both a will and a trust working together

- Simple estates under $1 million may only need a basic will, while complex estates benefit from trust-based planning

Understanding the Basics

What Is a Will?

A will is a legal document that tells the world what you want to happen to your property after you die. Think of it as your final instructions to your family and the courts. It names an executor to handle your affairs, specifies who gets your assets, and can designate guardians for minor children.

Wills only take effect after death and must go through probate court, where a judge validates the document and oversees asset distribution. This process is public, meaning anyone can see what you owned and who inherited it.

What Is a Trust?

A trust is like creating a special container for your assets while you’re still alive. You transfer ownership of your property to the trust, but as the trustee, you maintain complete control during your lifetime. When you die, a successor trustee takes over and distributes assets according to your instructions – no court involvement required.

The most common type is a revocable living trust, which you can change or cancel anytime. Unlike wills, trusts work immediately and continue operating after death without public disclosure.

The Probate Problem

Why Probate Matters

Probate is the legal process that validates wills and oversees asset distribution. While some small estates can use simplified procedures, most will-based estates face full probate court supervision. This means your family must present your will to a judge, prove its validity, inventory your assets, pay debts and taxes, and only then distribute what remains.

The process typically takes six months to two years, during which your beneficiaries can’t access inherited assets. Court filings become public record, so neighbors, creditors, and curious parties can see exactly what you owned and who got it.

The Real Cost of Probate

Probate expenses can cost between 3% and 7% of an estate’s value, including attorney fees, court costs, executor compensation, and appraisal fees. On a hypothetical $500,000 estate, families might pay $15,000 to $50,000 just for the privilege of distributing assets that already belong to them.

Beyond money, probate creates emotional stress during an already difficult time. Family members must deal with court deadlines, legal paperwork, and potential challenges from disgruntled relatives while grieving their loss.

When a Will Makes Sense

Simple Estates and Straightforward Goals

Wills work well for people with modest estates and uncomplicated family situations. If you own a home, some savings, and personal property worth less than $1 million total, a will might provide adequate protection without unnecessary complexity.

Wills are also essential for parents with minor children, as they’re the only way to legally name guardians. Even if you create a trust for financial assets, you’ll still need a will to specify who should raise your kids if something happens to you.

Cost and Simplicity Advantages

Creating a basic will costs much less than establishing a trust. Once created, wills require minimal ongoing maintenance unless your situation changes dramatically.

Wills are also easier to understand and modify. Most people can grasp how wills work without extensive legal education, making it simpler to explain your plans to family members.

When Trusts Offer Better Solutions

Complex Estates and Privacy Concerns

Trusts become more attractive as estates grow larger and more complex. If you own multiple properties, substantial investment accounts, or business interests, a trust can simplify management and distribution while providing valuable privacy protection.

High-profile estates demonstrate this benefit clearly. When celebrities die with only wills, their entire financial lives become tabloid fodder. Trust-based estates remain private, protecting family dignity and preventing unwanted attention.

Avoiding Probate Complications

Trust-based planning eliminates probate delays and costs. When you die, your successor trustee can immediately begin distributing assets according to your instructions. This proves especially valuable during emergencies when families need quick access to funds for living expenses or medical care.

Trusts also provide continuity if you become incapacitated. While wills only work after death, trusts continue operating if you can’t manage your affairs, allowing your successor trustee to handle finances without court intervention.

Special Situations That Require Careful Planning

Blended Families and Second Marriages

Trusts excel in complex family situations where you want to provide for a current spouse while preserving assets for children from previous relationships. A properly structured trust can give your spouse lifetime income while ensuring the principal eventually passes to your children.

Wills can’t provide this flexibility. They either give assets outright to beneficiaries or create complications that often end up in court.

Business Ownership and Professional Practices

If you own a business or professional practice, trusts can provide seamless succession planning. You can transfer business interests to a trust during your lifetime, maintain control as trustee, and specify exactly how ownership should transition after your death.

This approach prevents business disruption and protects employees, customers, and business value that might be lost during lengthy probate proceedings.

Children with Special Needs

Families with disabled children often need special needs trusts to provide financial support without disqualifying beneficiaries from government benefits like Medicaid or Social Security Disability. These trusts require careful drafting and ongoing administration that goes beyond what simple wills can accomplish.

The Best of Both Worlds

Why Many Families Need Both Documents

Most comprehensive estate plans include both wills and trusts working together. The trust handles major assets like real estate and investment accounts, while a “pour-over” will catches any assets accidentally left outside the trust and directs them into the trust after death.

This combination provides maximum flexibility. You get probate avoidance for trust assets, guardian nominations for children, and a safety net for anything you forgot to transfer to the trust.

Coordinating Your Estate Plan

Having both documents requires careful coordination to avoid conflicts. Your will and trust must work together seamlessly, with consistent beneficiary designations and clear instructions for your executors and trustees.

This coordination also extends to other estate planning documents like powers of attorney, advance directives, and beneficiary designations on retirement accounts and life insurance policies.

Making Your Decision

Factors to Consider

Your choice between a will and trust depends on several key factors: the size and complexity of your estate, your family situation, privacy concerns, and tolerance for ongoing administrative responsibilities. Trusts require more initial effort and cost but provide long-term benefits for many families.

Consider your specific circumstances carefully. Do you own property in multiple states? Have a complicated family structure? Value privacy highly? Want to provide ongoing management for beneficiaries? These factors point toward trust-based planning.

Getting Professional Help

While simple wills might be suitable for do-it-yourself approaches, trusts typically require professional assistance. An experienced estate planning attorney can evaluate your situation, recommend appropriate strategies, and ensure documents are properly drafted and coordinated.

The cost of professional help often proves minimal compared to the problems that arise from poorly planned estates or inadequate documentation.

Work With Us

The choice between a will and trust is about protecting your family’s future and ensuring your wishes are carried out efficiently and privately. With only 32% of Americans having a will and probate costs ranging from 3% to 7% of estate value, proper estate planning has never been more important. Whether your situation calls for a simple will, a comprehensive trust, or a combination of both depends on your unique circumstances, but delaying these decisions only creates more complications for your loved ones.

At Avior, we help clients develop comprehensive strategies that protect their wealth and family interests. Our team helps coordinate your estate planning with your overall financial plan, helping ensure your investment accounts, retirement savings, and tax strategies all work together to maximize what you leave behind. Whether you need guidance on funding a trust, coordinating beneficiary designations, or integrating estate planning with your retirement and tax strategies, we provide the comprehensive approach your family deserves. Contact Avior today to discuss how proper estate planning can protect your legacy and provide financial confidence for you and your loved ones.

Investment management and financial planning services are offered through Avior Wealth Management, LLC, an SEC-registered investment adviser. Tax and accounting services are provided by Avior Tax and Accounting, LLC, a wholly-owned subsidiary of Avior Wealth Management, LLC.

Insurance products, including life, disability, long-term care, and annuities, are offered through Avior Insurance. Insurance and annuity products are not offered through Avior Wealth Management, LLC, and are not covered by SIPC. Avior Insurance operates independently to provide insurance solutions tailored to clients’ needs. Insurance products are subject to the terms and conditions of the issuing carrier.

All information contained herein is general in nature and is not to be construed as specific investment advice. Avior does not provide legal advice. Clients should consult their own legal, tax, and financial professionals before making any decisions. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results.

No Comments

Sorry, the comment form is closed at this time.