AVIOR INSIGHTS – Navigating Bank Failures, Fed Rate Hikes, and Risks to the Financial System

The recent failure of three U.S. banks has raised concerns over the economy and financial system. The situation is still evolving and there is plenty of speculation as to what might come next. One recent development is that government officials from the Treasury, Federal Reserve, and FDIC have announced that depositors will be made whole in an effort to backstop the system and restore confidence. This crisis has already created hardship for many companies and individuals as payrolls are disrupted and access to cash is halted. However, when it comes to investing, it’s more important than ever to stay levelheaded and focus on the big picture. What should long-term investors know about these bank failures and what do they reveal about the financial system?

The collapse of Silicon Valley Bank (SVB) was the first FDIC-insured bank failure since 2020 and the second largest in history. This was followed two days later by the failure of Signature Bank, the third largest in history. Just a few weeks earlier, these two publicly traded companies had the 14th and 18th largest market capitalizations among U.S. banks, respectively. Silvergate, a smaller bank active in the crypto industry, also failed the same week, but through an orderly liquidation.

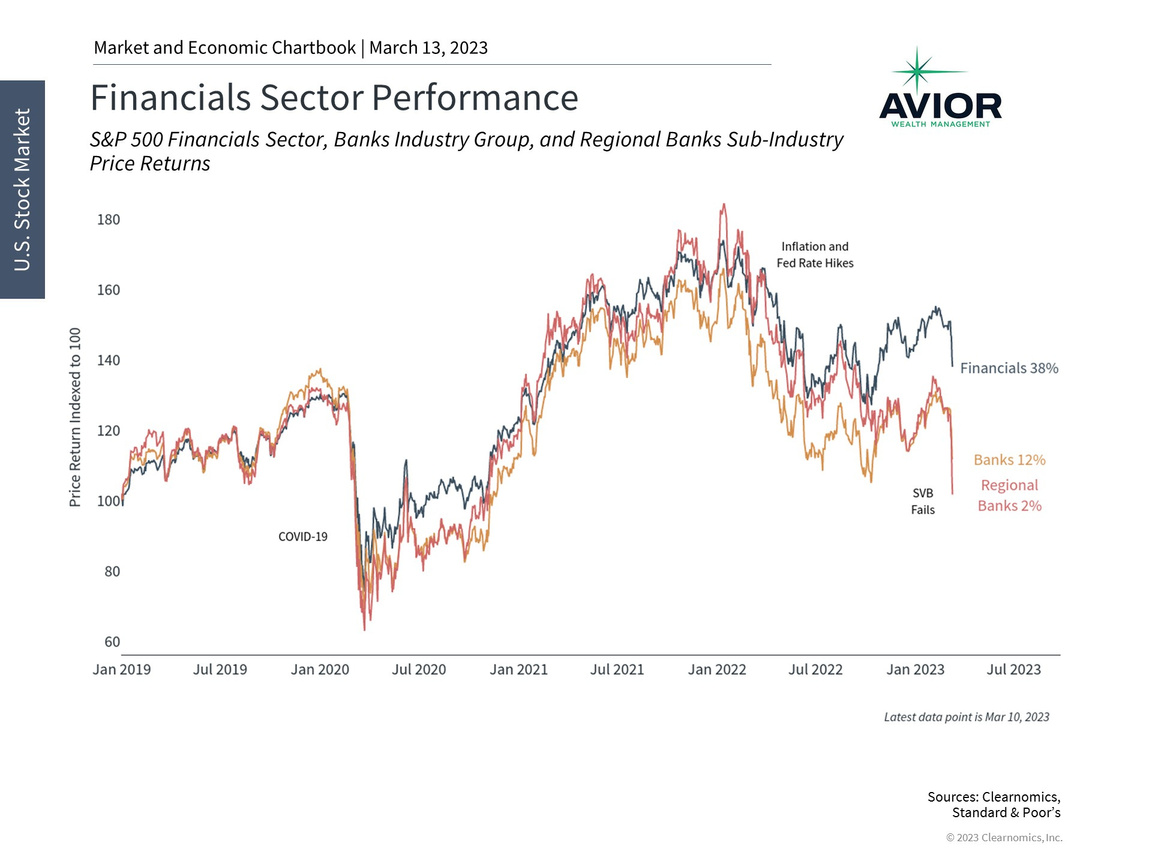

Bank stocks have struggled due to recent failures

From a market and economic perspective, the main question is whether there is wider systemic risk to the financial system. This episode reveals that these particular banks grew too aggressively and with too little risk management as tech valuations rose and crypto prices rallied over the past several years. While this worked well in a bull market, the reversal of these trends in 2022 made these banks vulnerable to classic bank runs.

How do bank runs occur? A simplified description of the classic banking model is that customers – both businesses and individuals – deposit funds for safekeeping. Banks then use these deposits to make loans or to buy high quality investment securities which they hope can generate profits. This works well as long as these investment assets maintain or grow in value and customers trust that their deposits are safe. If either of these is not the case, a bank may not have the liquidity to meet its obligations. With this in mind, these recent failures were due to two related problems.

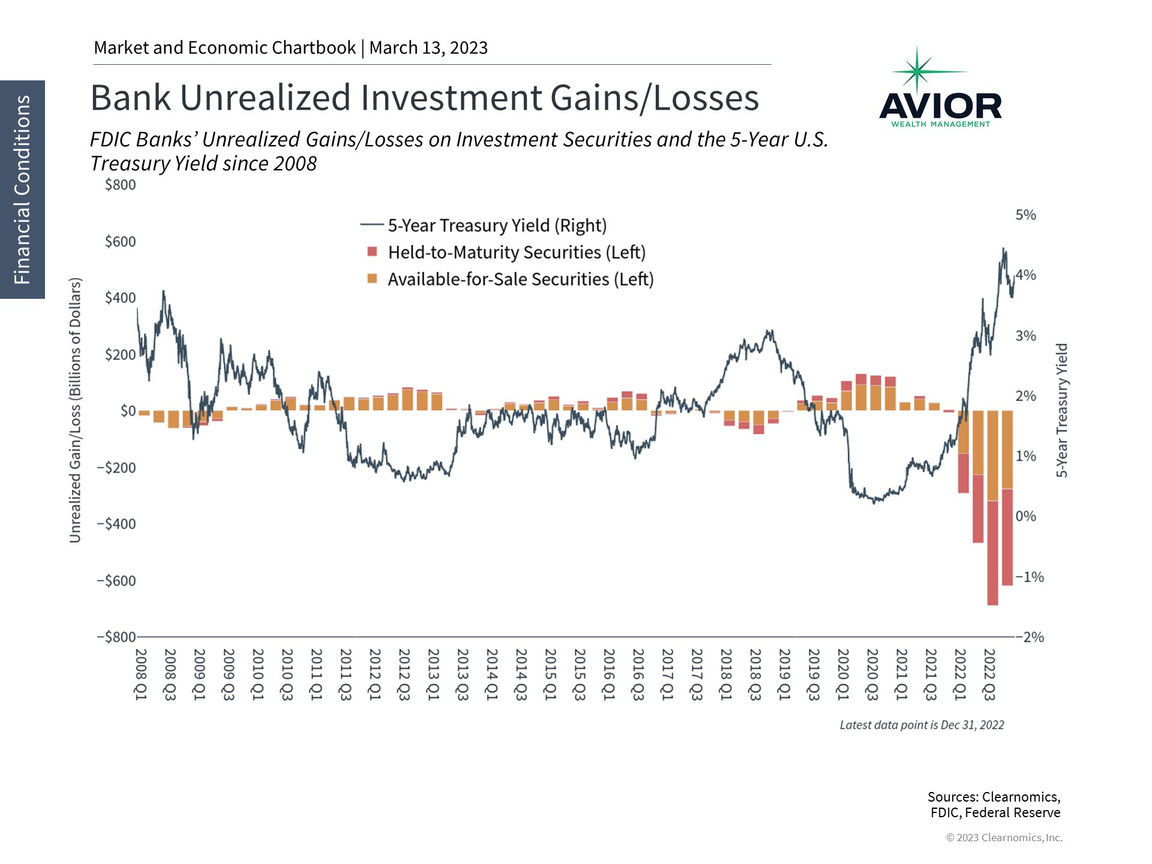

Banks accumulated unrealized losses on investment securities as rates spiked

First, rapidly rising interest rates and Fed rate hikes over the past year created financial stresses on bank balance sheets. Bonds had their worst performance in history in 2022, driving unrealized losses on investment assets including U.S. Treasuries, as shown in the accompanying chart. Whether banks need to book these losses depends on how these securities are accounted for, but this worsens as banks face pressure on deposits. Thus, SVB and others found themselves with assets that were worth far less as rates rose.

Second, SVB’s concentration of tech and startup customers made it vulnerable as conditions deteriorated for that sector, just as Silvergate and Signature Bank were exposed to the slowdown in the crypto industry. SVB tried to plug this gap by raising fresh capital, but this backfired since it highlighted the liquidity and solvency issues it faced. Like shouting “fire” in a crowded theater, once there is the perception of solvency problems, a classic bank run can occur swiftly, which can then become a self-fulfilling prophecy. To a large extent, this played out publicly as many in the startup and VC communities urged companies to move their funds.

While government actions are always controversial and subject to political debate, moves by Treasury, the Fed, and the FDIC to backstop customer deposits across these banks will likely help to prevent contagion effects across the system. At the same time, it does not directly address the underlying issue of impaired assets which depends on the quality of risk and asset/liability management at each bank. However, the risk that unrealized losses become a solvency issue is mitigated for larger, more diversified banks who are less reliant on deposits, have a stronger deposit base, and maintain higher amounts of capital.

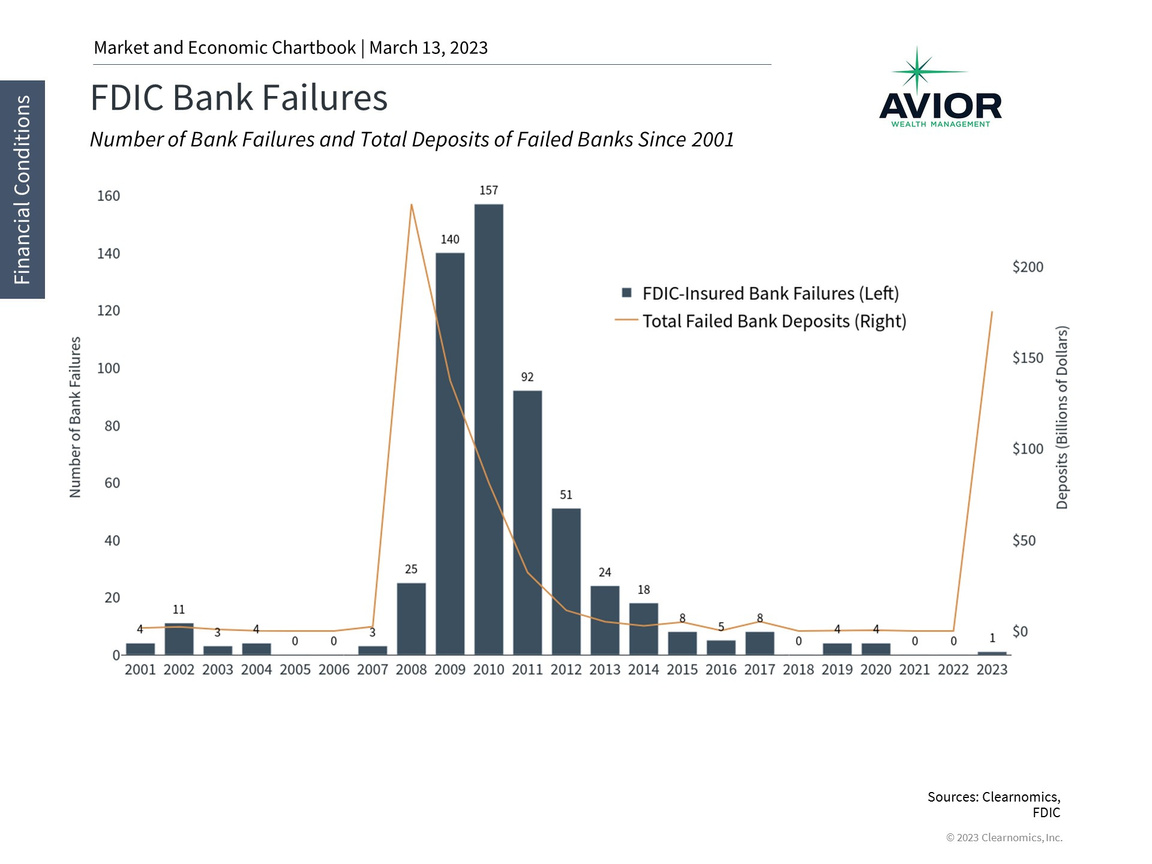

These bank failures are the largest since 2008

One reason that investors may be concerned is that there have been few bank failures in recent history, especially since banking legislation such as the Dodd-Frank Act was put into place after the 2008 financial crisis. According to the FDIC, there were only 8 bank failures from 2019 to 2022, far below the 322 experienced around the global financial crisis or the hundreds that regularly occurred in the 80s and 90s. That said, SVB is an outlier in that it had total deposits of $175 billion while the 8 from 2019 to 2022 had a combined $628 million.

Naturally, there are also parallels being drawn to 2008 when the last wave of bank failures threatened the global financial system. It’s important to keep in mind that, back then, the problem was not just that all banks held significant amounts of mortgage-backed securities and other housing-sensitive assets that ended up being worth only pennies on the dollar. Rather, significant amounts of leverage coupled with new financial instruments such as collateralized debt obligations allowed a housing crisis to turn into a financial meltdown. While it’s unclear exactly how this episode will play out, many banks today are much better capitalized and do not primarily rely on tech or crypto deposits. Additionally, any economic spillover has so far been concentrated in the technology and venture capital industries which were already struggling with layoffs and a slowdown in demand.

These developments impact the Fed’s upcoming rate decisions since they underscore an unintended consequence of rapid rate hikes. It’s likely that this creates a new sense of caution for the Fed as they continue to battle inflation. Based on market-based measures, investors no longer expect the Fed to raise rates again this year, but believe that there may be a rate cut by September. Interest rates have also fallen with the 2-year Treasury yield declining over one percentage point to around 4.1%. Ironically, this means that the very bonds with unrealized losses on bank balance sheets are now worth more. While these expectations can shift rapidly, they show how much sentiment has shifted in the past week.

The bottom line? While recent bank failures are problematic, parallels to 2008 are premature. Investors ought to stay diversified as the situation stabilizes, while focusing on the big picture rather than minute-by-minute speculation.

Disclosure: This report was obtained from Clearnomics, an unaffiliated third-party. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.avior.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments.

Avior Wealth Management, LLC, 14301 FNB Pkwy, Suite 110, Omaha, Nebraska 68154, United States, 402-218-4064

No Comments

Sorry, the comment form is closed at this time.