How to Align Beneficiary Designations With Your Estate Plan (Avoid These Mistakes)

A well-drafted will or trust can take months to finalize. You work with attorneys, weigh every scenario, and spell out exactly how you want your assets distributed. Then a single outdated beneficiary form on a retirement account quietly overrides all of it. That one form, often filled out years ago during a rushed HR onboarding session, may carry more legal weight than every carefully considered provision in your estate plan.

This disconnect catches families off guard more often than you might expect. According to a 2025 Caring.com survey, only 24% of American adults reported having a will, and the percentage who have reviewed their beneficiary designations recently is likely even smaller. When those designations fall out of sync with a will or trust, the results can range from unintended tax burdens to assets landing in the hands of an ex-spouse. The good news is that most of these mistakes are preventable with periodic reviews and a coordinated approach.

Key Takeaways

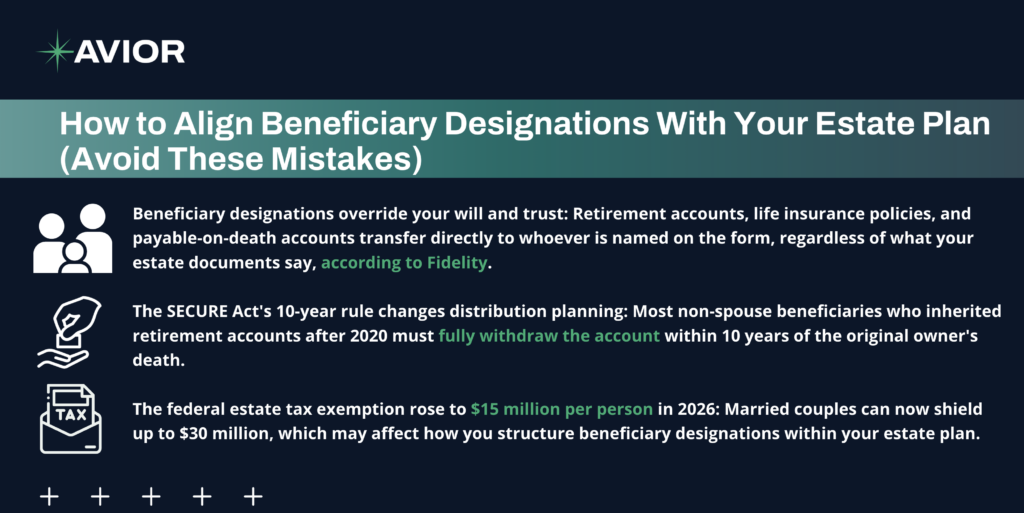

- Beneficiary designations override your will and trust: Retirement accounts, life insurance policies, and payable-on-death accounts transfer directly to whoever is named on the form, regardless of what your estate documents say, according to Fidelity.

- The SECURE Act’s 10-year rule changes distribution planning: Most non-spouse beneficiaries who inherited retirement accounts after 2020 must fully withdraw the account within 10 years of the original owner’s death.

- The federal estate tax exemption rose to $15 million per person in 2026: Married couples can now shield up to $30 million, which may affect how you structure beneficiary designations within your estate plan.

- Life events should trigger an immediate review: Marriage, divorce, the birth of a child, or the death of a named beneficiary are all moments when outdated forms could cause serious problems.

- Naming a minor child directly as a beneficiary can create legal complications: Courts may need to appoint a guardian to manage the funds, potentially delaying access and adding cost.

- Forgetting contingent beneficiaries could force assets into probate: If your primary beneficiary passes away before you and no backup is listed, the account may revert to your estate.

Why Beneficiary Designations Carry So Much Weight

Most people assume their will controls everything. It makes sense. You spent time and money drafting it, and your attorney walked you through every clause. But certain assets operate outside the will entirely. Retirement accounts like 401(k)s and IRAs, life insurance policies, annuities, and payable-on-death bank accounts all transfer based on the beneficiary designation form filed with the custodian or insurance company.

The Override Problem

That form you filled out when you first opened your 401(k) at age 28 could still be active decades later. If you named an ex-spouse as your primary beneficiary, got divorced, and never updated the form, your ex-spouse may legally receive those assets when you pass away. Your will can state otherwise in explicit terms, and it will likely lose that argument. Federal law, particularly ERISA for employer-sponsored retirement plans, generally gives the beneficiary designation form final say.

How This Creates Conflict

Consider a hypothetical scenario. A man remarries and updates his will to leave everything to his new wife and their children. His 401(k) from a previous employer still lists his first wife as the primary beneficiary. He passes away unexpectedly. The 401(k), which could represent a substantial portion of his estate, goes directly to his first wife. His current family may have limited legal recourse. This kind of situation unfolds quietly and often, because beneficiary forms tend to sit untouched for years.

Common Mistakes That Undermine Your Estate Plan

Failing to Update After Major Life Events

Divorce, remarriage, the birth of a child or grandchild, or the death of a named beneficiary all demand an immediate review of every account that carries a beneficiary designation. A Pew Research Center survey found that only about 32% of U.S. adults have created a will. The share who proactively review their beneficiary forms after life changes is likely far lower.

Naming Your Estate as the Beneficiary

This is a subtle mistake with outsized consequences. When you name your estate as the beneficiary of a retirement account, those funds get pulled into the probate process. Probate can be lengthy, expensive, and public. Worse, it may eliminate certain tax-advantaged distribution options that would otherwise be available to individual beneficiaries.

Overlooking Contingent Beneficiaries

Your primary beneficiary could pass away before you do. Without a contingent (secondary) beneficiary listed on the form, the account may default to your estate or follow the custodian’s plan rules, which might distribute assets in ways you never intended. Taking a few minutes to name a backup could save your family months of legal headaches.

Naming Minor Children Directly

If a minor is listed as a beneficiary, they cannot legally manage the funds. A court may need to appoint a custodian or guardian to oversee the assets until the child reaches adulthood. Setting up a trust to receive those assets on behalf of a minor may offer more flexibility, protection, and control over how the money gets used.

The SECURE Act and Its Impact on Beneficiary Planning

The SECURE Act of 2019 reshaped how inherited retirement accounts work, and the changes directly affect how you should think about beneficiary designations. Before 2020, non-spouse beneficiaries could stretch distributions from an inherited IRA over their own lifetime. The SECURE Act eliminated that option for most beneficiaries and replaced it with a 10-year distribution window.

Who Is Subject to the 10-Year Rule

Most non-spouse beneficiaries who inherit a retirement account from someone who passed away in 2020 or later must fully deplete the inherited account by the end of the 10th year following the account owner’s death. The IRS waived penalties for missed required minimum distributions from 2021 through 2024 while it finalized the rules, but those waivers ended in 2025. Failing to take required distributions now could trigger a 25% excise tax.

Exceptions Worth Knowing

Certain “eligible designated beneficiaries” are exempt from the 10-year rule and may still use life-expectancy-based distributions. This category includes a surviving spouse, a minor child of the account owner (until they reach age 21), someone who is disabled or chronically ill, and a beneficiary who is within 10 years of age of the original account owner. If one of your intended beneficiaries falls into these categories, the way you structure their designation could make a meaningful tax difference.

Coordinating Designations With Your Overall Estate Plan

Start With an Account Inventory

Gather every account that has a beneficiary designation: employer retirement plans, IRAs, Roth IRAs, life insurance policies, annuities, HSAs, and any bank or brokerage accounts with payable-on-death or transfer-on-death registrations. Write down who is currently listed as primary and contingent on each one. You may find surprises, particularly on older accounts from previous employers.

Match Designations to Your Will or Trust

Once you have your inventory, compare it against your estate planning documents. The goal is alignment. If your trust is designed to provide for your spouse during their lifetime and then distribute to your children, your beneficiary designations should reflect that structure. In some cases, it may make sense to name a trust as the beneficiary of a retirement account, particularly when you want to maintain control over how and when beneficiaries access the funds. This decision involves tax trade-offs, so working with a qualified advisor is a good idea before making changes.

Review at Least Annually

Estate planning professionals generally recommend reviewing beneficiary designations at least once a year, and always after a major life event. Think of it as routine maintenance. The same way you might review insurance coverage or rebalance an investment portfolio, a quick check of your beneficiary forms could prevent a costly misalignment down the road.

Tax Considerations You Should Keep in Mind

The federal estate tax exemption for 2026 is $15 million per individual, or $30 million for married couples, following the passage of the One Big Beautiful Bill Act. For most families, this means federal estate tax may not be a primary concern. But beneficiary designations still carry significant income tax implications, especially for retirement accounts funded with pre-tax dollars.

When a beneficiary inherits a traditional IRA or 401(k), withdrawals are taxed as ordinary income. The compressed 10-year distribution timeline under the SECURE Act could push heirs into higher tax brackets during those withdrawal years. A spousal beneficiary, on the other hand, may roll the inherited IRA into their own account and defer distributions based on their own timeline. These differences make the choice of beneficiary a planning decision with real financial impact.

Work With Us

Aligning beneficiary designations with your estate plan is one of the most practical steps you can take to protect your family’s financial future. A single outdated form has the power to redirect retirement savings, trigger unnecessary tax consequences, and create conflict among the people you care about most. Regular reviews, especially after life changes, and thoughtful coordination between your will, trusts, and account designations could help ensure your wishes are carried out the way you intend.

At Avior, we help clients bring every piece of their financial plan into alignment, from investment strategy to estate and tax planning. If you haven’t reviewed your beneficiary designations recently, or if a major life event has changed your circumstances, our team can help you identify gaps and build a coordinated plan. Schedule a consultation to take the next step toward protecting what matters most.

No Comments

Sorry, the comment form is closed at this time.