The Year-Round Tax Planning Calendar for Business Owners (What to Do Each Quarter)

Business owners who scramble every April to gather receipts and calculate tax obligations inevitably pay more than necessary, through missed deductions, late payment penalties, or simply failing to implement strategies that require advance planning. Tax planning works best when approached systematically throughout the year rather than compressed into a frantic pre-deadline rush.

The IRS structures estimated tax payments around four quarterly deadlines that anchor your tax planning calendar. Building comprehensive financial reviews around these payment dates helps ensure your books stay current, payroll remains compliant, and strategic opportunities get identified before deadlines eliminate them. This quarterly approach distributes work evenly across twelve months while creating natural checkpoints for evaluating business performance and tax position throughout the year.

Key Takeaways

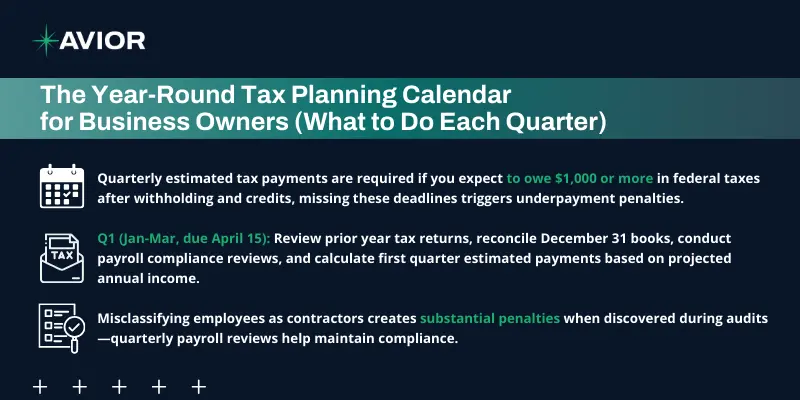

- Quarterly estimated tax payments are required if you expect to owe $1,000 or more in federal taxes after withholding and credits, missing these deadlines triggers underpayment penalties.

- Q1 (Jan-Mar, due April 15): Review prior year tax returns, reconcile December 31 books, conduct payroll compliance reviews, and calculate first quarter estimated payments based on projected annual income.

- Q2 (Apr-Jun, due June 15-16): File prior year returns, review first quarter financial performance, evaluate retirement plan options, and schedule mid-year tax planning sessions before year-end strategies become unavailable.

- Q3 (Jul-Sep, due September 15): Recalculate estimated payments based on actual year-to-date results, audit expense tracking and receipt organization, and begin planning year-end tax moves requiring advance implementation.

- Q4 (Oct-Dec, due January 15 following year): Maximize Section 179 equipment expensing and bonus depreciation, execute tax loss harvesting strategies, complete charitable contributions by December 31, and prepare W-2s for year-end processing.

- Misclassifying employees as contractors creates substantial penalties when discovered during audits—quarterly payroll reviews help maintain compliance.

Why Quarterly Planning Beats Year-End Scrambling

Annual tax planning compresses twelve months of strategic decisions into a few frantic December weeks. Quarterly planning distributes that work across the year, creating manageable checkpoints that align with IRS estimated payment deadlines.

This rhythm transforms tax management from crisis mode into routine business operations. You identify documentation gaps while correction remains possible. Strategic opportunities get evaluated before implementation deadlines pass. Cash flow planning improves when you anticipate tax payments months in advance rather than facing surprise bills in April.

Quarter 1: January Through March (Payment Due April 15)

The first quarter sets the foundation for your entire tax year. January provides a natural inflection point for implementing new strategies and establishing routines supporting year-round tax efficiency.

Review Prior Year Tax Returns

Begin by reviewing your previous year’s tax return with fresh eyes now that filing pressure has subsided. Identify areas where better documentation or different timing could have reduced tax liability. If large unexpected deductions or income items appeared, trace them back to understand what triggered them. This retrospective analysis reveals patterns you can leverage or avoid in the current year.

Calculate and Pay First Quarter Estimates

Quarterly estimated tax payments require attention if you expect to owe $1,000 or more in federal taxes after withholding and credits. Calculate your first quarter payment based on projected annual income. Business owners with irregular income benefit from the annualized income method, which bases each payment on actual year-to-date earnings rather than one-quarter of estimated annual tax.

The safe harbor rule protects you from underpayment penalties if you pay at least 100% of last year’s tax liability (110% if your prior year adjusted gross income exceeded $150,000). This approach provides certainty when projecting current year income feels impossible.

Reconcile Year-End Books

Reconcile your bookkeeping through December 31 to ensure prior year accuracy before your accountant begins tax preparation. Review profit and loss statements, verify all income and expense categorizations, and reconcile bank and credit card accounts. Missing this step creates delays when your tax professional requests information you should have organized months earlier.

Clean books accelerate tax preparation while reducing professional fees. Accountants spend less time hunting for missing transactions and more time identifying tax-saving strategies when your records arrive organized and complete.

Conduct Payroll Compliance Reviews

Verify proper employee classifications, accurate withholding calculations, and timely payroll tax deposits. Misclassifying employees as independent contractors creates substantial penalties when discovered during audits. The IRS examines whether you control what work gets done and how it gets done, if yes, that person is probably an employee regardless of what your agreement states.

Update employee W-4 forms annually to reflect life changes affecting withholding needs. Employees who got married, divorced, had children, or bought homes might need withholding adjustments to avoid surprise tax bills or excessive refunds.

Quarter 2: April Through June (Payment Due June 16)

The second quarter encompasses tax filing season, making it the busiest period for business owners juggling current operations with prior year compliance.

File Prior Year Returns and Make Second Payment

The second quarter payment deadline typically falls on June 15, though it shifts to June 16 when June 15 lands on a weekend. This compressed timeline between April 15 and mid-June requires extra attention to cash flow planning. You’re managing prior year tax payments, current quarter estimated payments, and ongoing business expenses simultaneously.

Review First Quarter Performance

Review first quarter financial performance against budget projections. Significant variances from anticipated income or expenses warrant revised annual estimates and potential adjustments to remaining estimated tax payments. Early identification of troubling trends provides more time to implement corrective measures before problems compound.

Compare revenue, gross margins, and operating expenses to both your budget and prior year first quarter. Patterns emerging in Q1 often persist throughout the year, making early identification valuable for course correction.

Evaluate Retirement Plan Contributions

Business owners have multiple retirement plan options, SEP IRAs, Solo 401(k)s, SIMPLE IRAs, each with different contribution limits, deadlines, and administrative requirements. The second quarter provides sufficient time to implement new plans while capturing current year tax benefits.

SEP IRAs offer simplicity with contribution deadlines extending to your tax filing deadline including extensions. Solo 401(k)s allow larger contributions through both employee deferrals and employer profit-sharing but require more administrative work. SIMPLE IRAs mandate employer contributions but work well for businesses with employees. Each structure fits different business situations.

Schedule Mid-Year Tax Planning Sessions

Conduct mid-year tax planning meetings with your accountant. Waiting until year-end to discuss tax strategy eliminates many beneficial moves requiring implementation before specific dates. Capital equipment purchases qualifying for Section 179 expensing, Roth conversion strategies, charitable giving plans, and income deferral techniques all benefit from mid-year consideration.

These conversations reveal whether your year is tracking as expected or if adjustments are needed. Your accountant can project year-end tax liability based on six months of actual results, providing more accurate planning than January projections based on assumptions.

Quarter 3: July Through September (Payment Due September 15)

The third quarter represents peak business activity for many industries, making systematic financial management critical when operational demands intensify.

Recalculate Third Quarter Payments

September 15 marks your third estimated payment deadline. Recalculate required payments based on actual year-to-date results rather than initial projections made nine months earlier. Significant income increases warrant higher third quarter payments to avoid underpayment penalties, while declining revenues might justify reduced estimates.

The annualized income method becomes particularly valuable in Q3. If your business has seasonal patterns, landscape companies earning most revenue in spring and summer, retail businesses peaking in Q4, annualizing lets you match payments to actual earnings rather than forcing equal quarterly payments.

Review Accounts Receivable and Collections

Review accounts receivable aging to identify collection issues before they become problematic. Cash-basis taxpayers can sometimes time year-end income recognition through strategic collection efforts or delays, providing tools for managing current year taxable income.

Invoices over 60 days past due warrant immediate attention. Collection problems identified in September leave time for resolution before year-end affects your tax and financial position. Clean accounts receivable also improve your business’s financial standing for potential financing needs.

Audit Expense Tracking and Receipt Organization

Audit your expense tracking and receipt organization. Missing documentation undermines legitimate deductions during tax preparation or IRS examinations. Implement quarterly receipt reconciliation—matching credit card and bank transactions to saved receipts—rather than waiting until January when memories fade and documents disappear.

Cloud-based accounting software with receipt capture features reduces documentation burdens. Mobile apps let you photograph receipts immediately, attaching them to transactions before you lose the paper copy. This technology eliminates shoeboxes full of fading receipts while improving deduction substantiation.

Begin Year-End Planning for Complex Strategies

Consider year-end tax moves requiring advance planning. Qualified opportunity zone investments, installment sales, like-kind exchanges, and various business succession strategies all require careful structuring and documentation that cannot be rushed in December. Third quarter planning meetings identify these opportunities while leaving adequate implementation time.

Business sales, partner buyouts, and entity restructurings all carry significant tax implications requiring months of planning. Starting these conversations in Q3 allows proper structuring rather than forcing rushed decisions that might increase tax costs.

Quarter 4: October Through December (Payment Due January 15 Following Year)

The final quarter combines year-end planning with preparation for the upcoming filing season.

Calculate Fourth Quarter Payment

The fourth quarter payment deadline falls on January 15 of the following year, giving you a brief window after year-end to calculate final payment amounts based on actual results. Some businesses can skip this payment by filing complete returns and paying all taxes owed by the end of January, though most lack the tax documents needed for such early filing.

This January 15 deadline creates strategic flexibility. You can calculate fourth quarter payments with complete year-end financial data rather than December estimates. However, waiting until January to pay means managing larger cash outlays when businesses often face post-holiday cash flow constraints.

Maximize Year-End Deductible Spending

Maximize tax-advantaged spending before December 31. Section 179 equipment expensing and bonus depreciation allow immediate deduction of qualifying asset purchases placed in service by year-end. For 2025, Section 179 expensing allows up to $1,220,000 in immediate deductions for qualifying equipment purchases (though this phases out for very large purchase volumes).

Medical and dental expenses paid before December 31 count toward current year deductions if you itemize. Charitable contributions require completion by year-end, with special rules for donor-advised funds and qualified charitable distributions from IRAs.

The key is distinguishing between expenses benefiting current year taxes and those that don’t. Prepaying 2026 expenses rarely accelerates deductions, while purchasing needed equipment in December rather than January can generate current year tax savings.

Review Employee Benefits and Prepare Year-End Processing

Review employee benefits and prepare for year-end processing. W-2 preparation requires accurate wage tracking, benefits valuations, and verification of payroll tax deposits. Health Savings Account contributions, flexible spending account elections, and retirement plan deferrals all face year-end deadlines affecting both current year taxes and employee benefits.

Beginning this review in October rather than December reduces errors and identifies issues while correction remains possible. Employees appreciate advance notice about benefit elections and year-end deadlines rather than rushed December communications.

Execute Year-End Tax Strategies

Execute year-end tax strategy decisions identified in earlier quarters. Tax loss harvesting to offset capital gains, accelerated expenses, deferred income, retirement plan contributions up to plan limits, and various credits requiring specific year-end actions all demand attention before December 31.

These moves cannot be retroactively implemented after year-end passes. A stock sale generating capital gains requires offsetting losses before December 31. Retirement contributions for many plans must occur by year-end rather than extending to the tax filing deadline. Charitable contributions using appreciated stock need time for broker transfers to complete.

Organize Documents and Schedule Tax Appointments

Prepare for the upcoming filing season by organizing documents, updating your document management system, and scheduling your tax preparation appointment well in advance of the April deadline. Tax professionals experience extreme workload compression in February and March.

Early appointments ensure adequate time for thorough preparation and strategic discussions rather than rushed filing focused solely on compliance. Scheduling your February appointment in November guarantees availability when your preferred preparer’s calendar fills quickly.

Monthly Habits Supporting Quarterly Success

Quarterly planning works best when supported by consistent monthly practices that maintain accurate records and identify issues early.

Reconcile Bank and Credit Card Accounts

Monthly reconciliation catches errors, fraudulent transactions, and missing deposits before they compound. Waiting until quarter-end to reconcile three months of transactions creates frustration and increases the likelihood of missing problems. Ten minutes monthly beats hours quarterly while improving accuracy.

Review Profit and Loss Statements

Monthly P&L review helps you spot revenue trends, expense creep, and unusual transactions requiring investigation. Comparing actual results to budget each month keeps you aware of business performance rather than discovering problems months later during quarterly reviews.

Track Mileage and Receipts Contemporaneously

Log business mileage when trips occur rather than reconstructing months later. Photograph receipts immediately using smartphone apps that capture and categorize expenses automatically. Contemporary documentation satisfies IRS substantiation requirements while reducing year-end stress.

Work With Us

Managing business taxes effectively requires a year-round quarterly approach rather than annual scrambling. Each quarter brings specific deadlines, estimated tax payments, bookkeeping reconciliation, payroll reviews, and strategic planning windows, that together create a systematic tax management framework. This distributed approach smooths workload, identifies tax-saving opportunities before implementation deadlines pass, maintains cleaner books, and reduces the stress associated with compressed year-end planning.

At Avior, we help business owners integrate tax planning with overall financial strategy to minimize lifetime tax costs while building wealth through their businesses. Our approach coordinates quarterly tax planning with cash flow management, retirement savings, business succession planning, and personal financial goals to create comprehensive strategies aligned with your priorities. Schedule a consultation with our team to discuss implementing a systematic quarterly tax planning calendar customized for your business structure and goals.

No Comments

Sorry, the comment form is closed at this time.